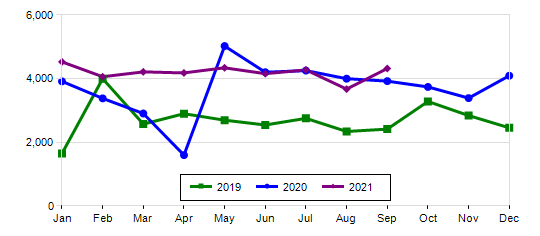

Home Equity Conversion Mortgage (HECM) endorsements fell slightly in November 2021 by 1.5% to 4,953 loans, a modest hit that still makes November the second-highest volume month of the year after the threshold of over 5,000 loans reached in October. This is according to data compiled by Reverse Market Insight (RMI).

While July may have marked the end of a streak of monthly volume above a threshold of at least 4,000 units that the industry had seen since late 2020, September’s volume spike managed to overcome the shortfall observed in August completely. October’s succeeding volume levels have put the industry back into a solid position, and the slight reduction seen in November does little to tamp down endorsement momentum observed since the beginning of the fall.

Once more, the production of new Home Equity Conversion Mortgage (HECM)-backed securities (HMBS) recorded a record $1.2 billion in HMBS issuance in the ninth month of the period after the London Interbank Offered Rate (LIBOR) “era.” Prior year records, as expected, fell in November since a total of $11.7 billion in HMBS issued so far this year has overtaken the previous industry record set in 2010, according to publicly available Ginnie Mae data and private sources compiled by New View Advisors.

All told, 2020 saw $10.6 billion in total HMBS issuance, eclipsing a recent industry high of $10.5 billion of issuance in 2017.

Reverse mortgage volume remains solid as the year’s end approaches

Even when looking beyond raw volume numbers, industry fundamentals appear strong as we prepare to say goodbye to 2021 according to John Lunde, president of RMI.

“It’s been a very positive year for the reverse mortgage industry in terms of volume, both at loan unit and securitization volume levels,” he told RMD. “There have been some challenges in terms of HMBS premium levels in the past few months, but that’s somewhat expected given the dependence on securitization and volatility in financial markets.”

The biggest risk to industry momentum at the end of the year and into 2022 remains the prevalence of HECM-to-HECM refinances as a sizable share of total loan volume, Lunde says. However, with the recent announcement of a 2022 reverse mortgage lending limit of very nearly $1 million, that risk is slightly diminished.

“The dependence on HECM-to-HECM refinance volumes has been the biggest potential risk to production volume moving forward, but with the lending limit increase there’s less risk in that niche than last week,” he said. “There may be some short-term volatility since consumers and lenders in homes near the 2021 limits might be better served to wait until after January 1 [to take advantage of higher lending limits], but that’s a blip more than anything and wouldn’t show up in endorsements until Q1 anyway.”

Lenders making moves, likelihood of a December swerve

Perhaps more interesting in terms of lender performance are the big swings made beyond the top 10, Lunde says. While half of the top 10 lenders saw volume reductions this month, lenders in the 11-20 positions saw year-to-date increases of well over 100%.

“In many ways it’s easier to show higher growth rates off a smaller base, but 4 of those 10 lenders doubling or more year-to-date is impressive,” Lunde says. “The challenge is there’s a significant drop off in volume level from 7 to 8, then 8 to 9, and again 9 to 10. The gap from 10 to 17 is less than from 9 to 10, so there are several lenders that could jump into that 10 spot with sustained performance next year, or perhaps number 9, but there are so many contenders there that it will be a great race to watch.”

When asked if it was possible for December’s volume to swerve into an unexpected direction that bucks recent trends, Lunde pulled data that indicated that it has happened recently before. However, circumstances this year are arguably a bit different.

“We’ve actually seen the past two years diverge considerably in December, with 2019 coasting down to finish before bouncing up in January 2020, while December 2020 hit a high note before the industry struggled in the first 4 months of this year,” Lunde explains. “Some of that is the noise from the election cycle dominating consumer attention and crowding out reverse mortgage advertising, but in general it wouldn’t be unusual to see a bit of slow down with holiday time off for both consumers and industry. That said, this year has been above 2020 almost every month so I expect continued momentum into 2022.”

HMBS volume record broken

With a long-predicted fall of the HMBS issuance record from 2010 finally taking place in November, a few specific things will need to continue in terms of industry activity for HMBS momentum to continue well into next year. This is according to Michael McCully, partner at New View Advisors.

However, if the industry momentum does continue, proprietary reverse mortgage volume may take a hit, he adds. Proprietary reverse mortgages are most typically designed to serve borrowers who own higher-value homes of up to $4 million. For a borrower who owns a home at or near the new HECM lending limit of $970,800, borrowers may seek the time-honored, government-sponsored reverse mortgage product variation instead of a private product when the new limits go into effect.

“Interest rates need to remain low, and home values stable for this level of volume to continue,” he told RMD. “The new maximum claim amount (MCA) limits going into effect in January will give the industry another boost, albeit at the expense of private product production.”

Tail HMBS issuance of $148 million did show lower-than-average in November, and tail pools are essential for “issuers to finance their monthly advances, such as borrower draws and FHA mortgage insurance premiums,” New View said in its commentary accompanying the data. When asked if this could present concern, McCully described the lower figure as an artifact of higher refinance volume.

“Current lower tail issuance reflects increased refinance activity,” McCully said. “Because meaningful tail issuance does not begin until utilization caps expire, HECMs refinanced prior to then cannot contribute to tail issuance volume.”

All told, the industry has absorbed the product changes handed down in between 2015 and 2017 by the Obama and Trump administrations rather well, McCully says, and such changes are having a positive impact on the HMBS side of the equation.

“We’re pleased to see the positive impact lower PLFs, financial assessment, lowering the expected minimum rate and other program improvements have had since 2015,” McCully said. “Defaults remain low, and interest accretion has slowed, reducing the number of underwater HECMs, and HECMs assigned to HUD. These program changes will have a lasting, long-term positive impact on the industry.”

Read the HECM Lenders report at RMI, and the HMBS Issuance report at New View Advisors.