Last week at REO Expo 2010—a conference led by HousingWire‘s sister publication REO Insider—I had the great pleasure of not only listening to Beacon Economics’ Christopher Thornberg, but also being able to speak with him off the record both before and after his keynote address.

By the way, for those of you who missed his talk, you can access the slides here.

Thornberg essentially noted in his speech that while the recession is over, for now, we’re not there yet in terms of a sustainable economic recovery. He exhorted attendees to enjoy 2010, as he expects the year to be a relatively good one compared to what we may see in 2011 and 2012.

Notice I said relatively good. I suspect that for most Americans, things don’t feel all that great despite news of economic recovery.

After all, the backlog of foreclosures remains substantial—and while the pace of delinquencies are slowing, the rate at which mortgages are going sour remains well above historical norms. Millions of borrowers are underwater, owing more on their mortgage debt than their homes are worth. The recent surge in housing, owing largely to tax credit-induced stimulus, has already worn off—leaving most analysts predicting a rough back half of this year for housing.

We already know that ridiculously low mortgage rates aren’t enough on their own to support housing demand: witness purchase applications falling off a cliff post-tax credit, while refinance demand has been tepid at best.

Retail sales, the most basic barometer of economic health, faltered unexpectedly in May as building material spending dropped off a cliff. Even in auto sales, the chorus of the recent economic rallying cry, questions are starting to emerge as data is emerging suggesting that the recovery in auto sales has far less to do with consumers than originally thought.

The most recent jobs data caught the Street off guard last week, too—most economists I know of, including Mark Zandi at Moody’s Analytics, expect we won’t see a 5.5 percent unemployment rate until at least 2015. And as jobs go, so too tends to go housing (sans the post-tech bubble era of mortgage finance, where we witnessed a jobless recovery and a historic run-up in housing prices that likely won’t be repeated again).

What does it all mean? It adds up to some economic pain ahead, and it might be far sooner than many of us think. One economic think-tank I’ve been introduced to recently is the Consumer Metrics Institute — the company tracks consumer discretionary spending on a daily basis, and is well worth a subscription.

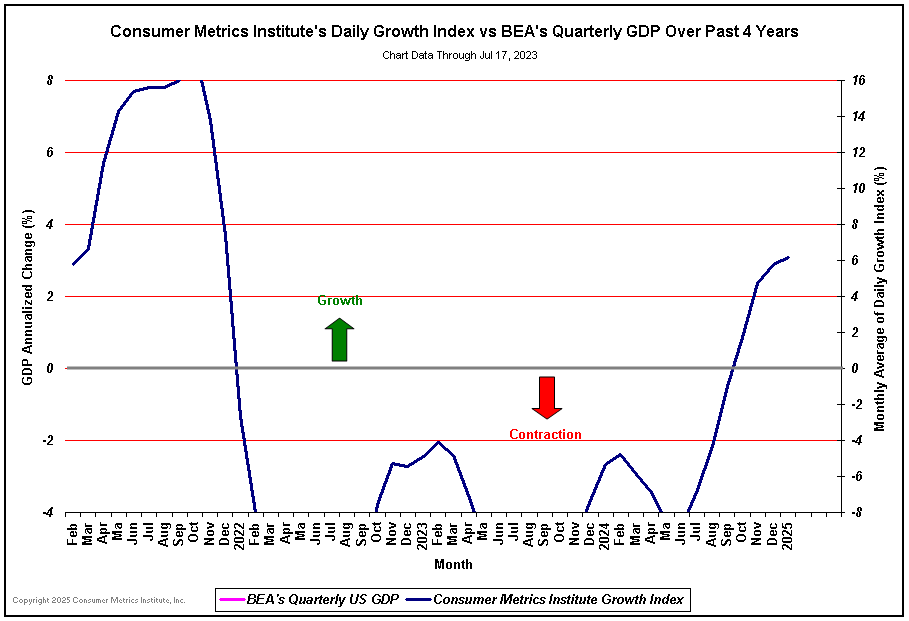

Their unique index has a pretty good track record of being a true leading indicator of GDP direction, something that should earn this firm an incredible amount of notoriety beyond the financial elite. Check out the below graph:

Pay close attention to the above — the CMI daily growth index is calling for a -2.0 GDP growth rate in the third quarter of this year. The general economic consensus right now is for a 3.0% growth rate. Given some of the data I mentioned above, I have a sneaking feeling that many of the current estimates are in for a pretty steep downward revision in the months ahead.

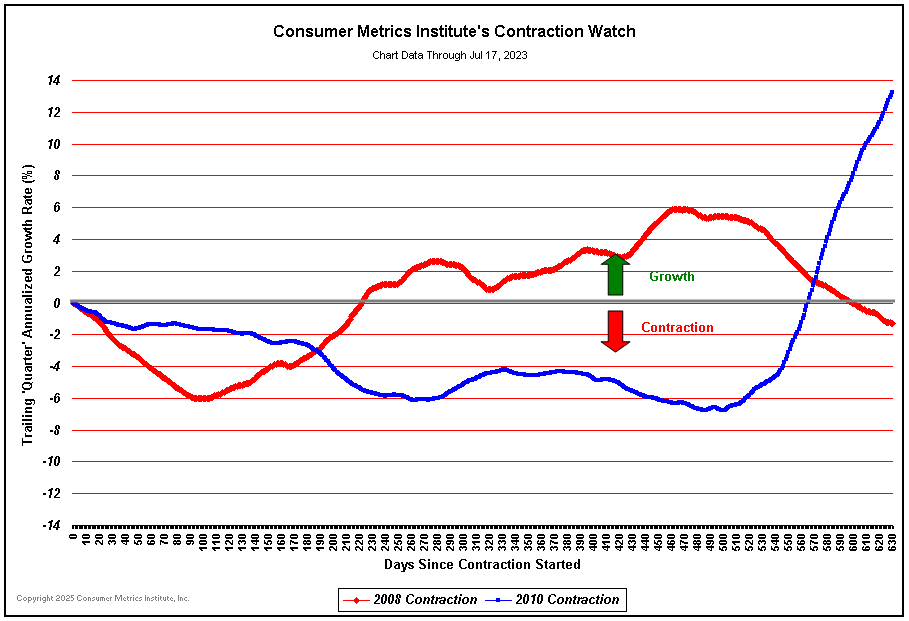

The CMI folks have been calling a contraction in consumer demand since the start of 2010, and most recently have noted just how ‘weird’ the current slowdown is relative to previous consumer demand contraction events. Here’s a look at the data:

From CMI’s Richard Davis, commenting on the consumer demand data:

“What is troubling to our eyes is that the shape of the current curve is clearly different from both the 2006 and 2008 events, which were similar except for scale. Put bluntly, our recent past experience with contraction events can offer no predictions as to where we are headed now. Something is structurally different this time.”

Gluskin Sheff economist David Rosenberg got in on this game in a Monday letter earlier today, as well, musing the following in analyzing retail sales numbers: “Maybe something funky is starting to go down here.”

Maybe so. A Harvard University study noted today that real median U.S. household incomes are likely to end this decade lower than when we started — a trend that, if it comes to pass, will have lasting and substantial impact on demand for U.S. housing.

For his part, Rosenberg came out firing today, noting that key data now projects an 80% likelihood of a double-dip recession — I’ll spare readers the technicals here for brevity’s sake. But Rosenberg is now projecting the very real possibility of a negative GDP print as soon as Q4 of this year. Expect others to begin to follow his thinking shortly.

I personally wouldn’t be surprised to see us jump back into the red one quarter earlier; that said, we still have substantial amount of unspent stimulus in the system that may yet keep this patient alive a few months longer.

In the end, whether later this year or early next, this means that the recent broad decreases in delinquencies (and associated involuntary prepayments) — just like the tax-credit fueled home price boost before it — will likely prove to be a short-lived phenomenon.

Paul Jackson is the publisher of HousingWire.com and HousingWire Magazine. Follow him on Twitter: @pjackson