In June of this year, I raised the fifth recession red flag, putting the housing market in a traditional recession where sales, incomes, jobs, and production would be falling, which is happening now. And unfortunately, one of those productions items is housing completions data — which looks terrible in the latest report.

As someone concerned about the housing inflation story since inventory channels broke to all-time lows in 2020, I am frustrated by this housing completion data. The best way to deal with housing inflation is more supply. If you’re reduced to fighting inflation by demand destruction, you’ve already lost the battle because either you had a massive credit boom, which we didn’t, or you didn’t have enough product supply for the consumer. All housing inventory data points to the second factor.

From Census: Housing Completions Privately owned housing completions in September were at a seasonally adjusted annual rate of 1,427,000. This is 6.1 percent (±11.0 percent)* above the revised August estimate of 1,345,000 and is 15.7 percent (±13.1 percent) above the September 2021 rate of 1,233,000. Single-family housing completions in September were at a rate of 1,049,000; this is 3.2 percent (±8.8 percent)* above the revised August rate of 1,016,000. The September rate for units in buildings with five units or more was 376,000.

As you can see below, during the housing bubble years, housing starts, permits, sales, credit, prices and housing completions moved together in 2005 to form the peak of the housing bubble. In the past several years, due to COVID-19 at first, the ability to close homes on time became an issue. Now, I believe that the builders are taking their time to finish the construction of new homes, especially those they haven’t even started, because they know demand will get hit big time with mortgage rates up.

The new home sales market gets hit harder by higher mortgage rates than the existing home market. The new home sale market a much smaller marketplace, but it has an outsized impact on the economy because of construction jobs, big-ticket item purchases, and all the income made building and selling a new home. This is why when I went on CNBC a few months ago, I talked about how we are in a traditional housing recession.

As the housing market worsened, the need to build single-family housing started to disappear. Remember, the builders don’t build homes to lose money; they build homes to make money. They do not care about inventory levels being near record lows in the existing home sales marketplace. That is their competition, so once the demand is hit, they pull back.

NAR total Inventory data: Traditionally, we have 2 million to 2.5 million, currently we are at 1.28 million.

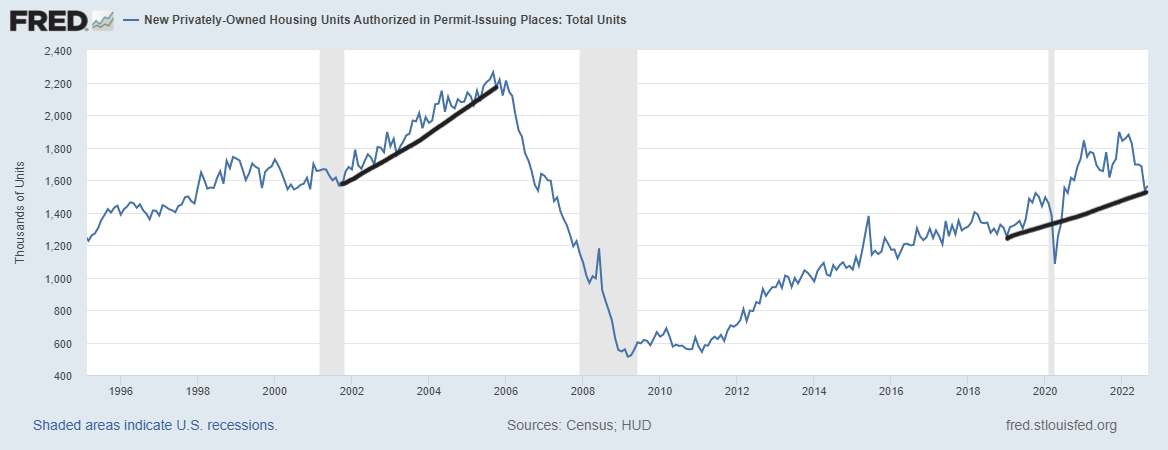

From Census: Housing Starts Privately-owned housing starts in September were at a seasonally adjusted annual rate of 1,439,000. This is 8.1 percent (±14.9 percent)* below the revised August estimate of 1,566,000 and is 7.7 percent (±11.5 percent)* below the September 2021 rate of 1,559,000. Single-family housing starts in September were at a rate of 892,000; this is 4.7 percent (±10.7 percent)* below the revised August figure of 936,000. The September rate for units in buildings with five units or more was 530,000.

Single-family starts are falling more noticeably, as they should. The builders must protect their profit margins as much as possible during a housing recession. Traditionally what turns this is lower mortgage rates, and that isn’t the case anymore. Mortgage rates being over 7% is a big issue for builders.

Housing starts have held up just a tad better as two-unit construction is still positive for the year and rental vacancy data is still low historically in America. However, if that segment of the economy starts to show softness, as we have seen in some parts of the U.S., the future of housing is that it can fall even more.

From Census: Building Permits Privately-owned housing units authorized by building permits in September were at a seasonally adjusted annual rate of 1,564,000. This is 1.4 percent above the revised August rate of 1,542,000, but is 3.2 percent below the September 2021 rate of 1,615,000. Single-family authorizations in September were at a rate of 872,000; this is 3.1 percent below the revised August figure of 900,000. Authorizations of units in buildings with five units or more were at a rate of 644,000 in September.

Building permits grew just a little month to month due to prior months’ data having negative revisions; even though single-family starts look very weak, the builders haven’t given up on two-unit construction just yet. We have 910,000 two-unit buildings under construction; let’s get these buildings out to fight inflation! If we get rental inflation to fall, that will be a plus for lower mortgage rates in 2023.

How to know when things will turn for the better in this housing sector

Traditionally, mortgage rates have to head lower. That has always worked in the past because it gives builders confidence to build, but the builder’s confidence data now is collapsing. When things turn, the NAHB/Wells Fargo Housing Market Index builder’s confidence data will let you know. It is the most efficient survey we have in U.S. economics because it’s based on profits rather than ideological takes.

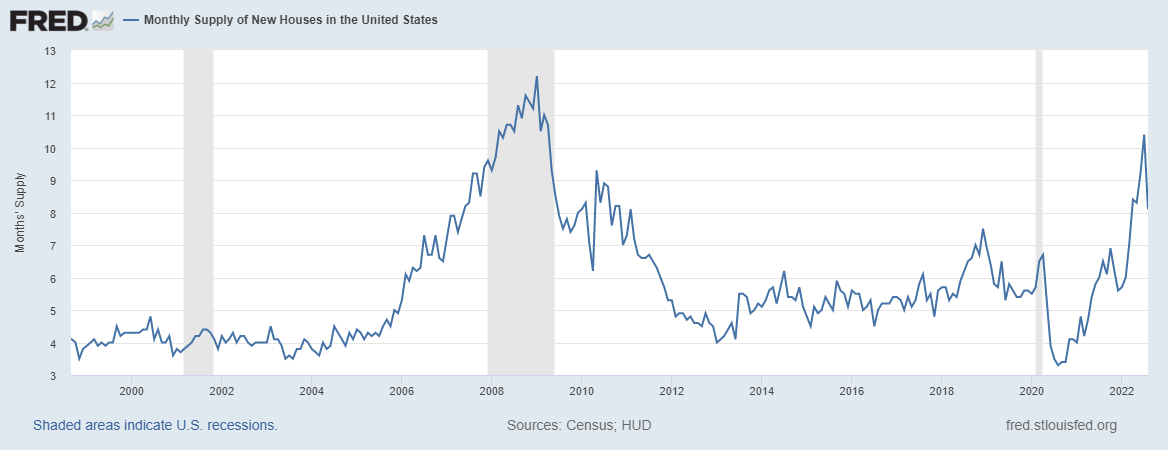

Another way to know things are getting better is by looking at the monthly supply numbers from the new home sales data. My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is just an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

The last month’s new home sales report was abnormally strong, driving down monthly supply from 10.9 months to 8.1 months. I wrote that we should take that report with a grain of salt. However, as we can see below, we still have some work to do on the supply front for the builders

As you can see above, the best way to fight housing inflation, and the growth rate of rent is to get all those two-units in construction onto the marketplace and force the growth rate of rents to cool down. Once we can get the housing completion data looking better, the growth rate of rent — which is the biggest driver of core CPI — can cool down.

With the growth rate of inflation falling, then the Federal Reserve and the bond market can be more productive in getting mortgage rates lower, which will help the housing market with more demand for purchases and refinancing.

Getting the two-unit buildings in-process onto the market is a very short-term solution if the volume of starts stays flat or diminishes.

Still, with the growth rate of rent falling in some of the more recent data line trackers, with more 2-unit supply coming into the market, that will filter into the CPI data more toward the end of 2023.