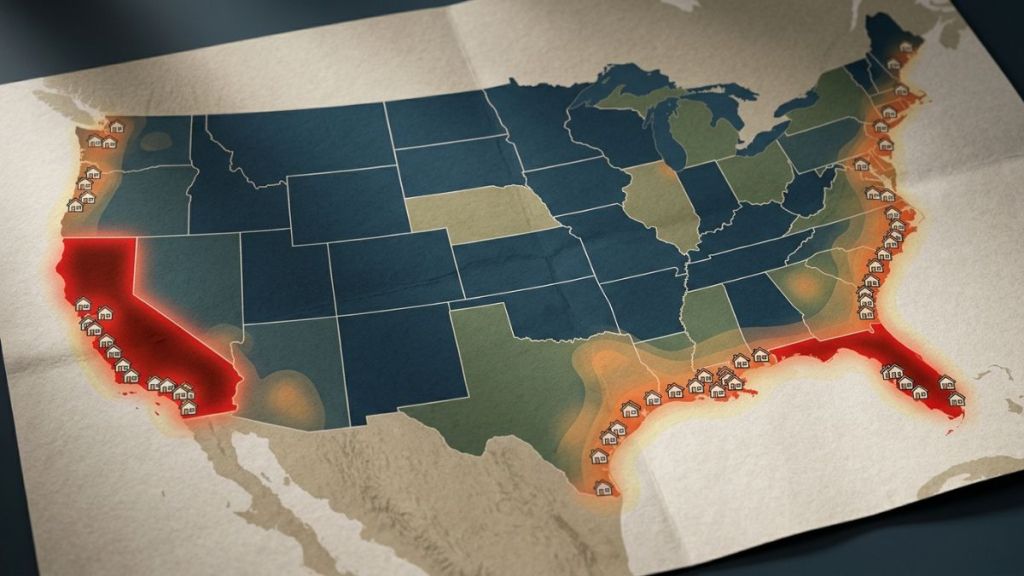

Unemployment and foreclosure activity were the primary drivers of housing market risk in the first quarter of 2026, with clusters of vulnerable counties in Florida and California along with safer markets concentrated in Tennessee, according to ATTOM‘s Housing Impact Report released Thursday.

ATTOM’s county-level analysis ranked 580 U.S. housing markets on four factors — the share of homes in foreclosure; the percentage of mortgages that are seriously underwater; affordability based on local wages and median prices; and local unemployment rates.

Of the 50 riskiest counties, 12 were in Florida, nine were in California and five each were in Illinois and New Jersey, ATTOM reports. The counties deemed most vulnerable overall were Charlotte County, Florida; Butte County, California; Charles County, Maryland; Shasta County, California; and Cumberland County, New Jersey.

ATTOM CEO Rob Barber said risk was concentrated where unemployment rates have climbed above 5% and distress indicators are highest, even as home prices have leveled off from 2025 peaks.

The report gives mortgage lenders and servicers, along with real estate investors and agents, a map for where credit risk, distressed inventory and affordability pressures are most likely to surface as markets digest higher interest rates and a softening labor market. The findings can inform underwriting standards, pricing, portfolio concentration limits, and branch or marketing strategies at the local level.

Tennessee markets among the safest

At the opposite end of the spectrum, ATTOM identified clusters of counties with relatively low housing risk.

- Safest counties overall: Chittenden County, Vermont; Rutherford County, Tennessee; Arlington County, Virginia; Tippecanoe County, Indiana; and Cumberland County, Maine had the lowest composite risk scores.

- Geographic concentration: Among the 50 least risky counties, nine were in Tennessee, five each were in Virginia and Wisconsin, and four were in Michigan.

These markets were not substantially more affordable than others, but they posted some of the lowest unemployment and foreclosure rates in the country and had relatively low shares of underwater mortgages, ATTOM said.

For lenders and investors, these patterns point to where credit performance and home price resiliency may be stronger in a downturn, even if affordability remains stretched.

Broad-based affordability pressures

ATTOM reported that in the first quarter of 2026, the national median home sales price was $360,000. At that price level, major monthly ownership costs would consume 30.3% of the typical American worker’s annual wages.

Several high-cost coastal markets stood out as especially unaffordable:

- Kings County, New York (Brooklyn): Ownership costs for a median-priced home would consume 108.6% of the typical local wage

- Santa Cruz County, California: 97.1%

- Marin County, California: 91.1%

- San Luis Obispo County, California: 89.7%

- Orange County, California: 88.1%

These numbers underscore that in several large coastal employment centers, homeownership at current pricing remains functionally out of reach for median-wage households. This is a factor that can support rental demand while also limiting owner-occupied purchase volume.

Underwater mortgages concentrated in Louisiana

Nationwide, 3.2% of homes were considered seriously underwater in Q1 2026, meaning their combined loan balances were at least 25% higher than the property’s estimated market value.

All five counties with the highest incidence of seriously underwater homes were in Louisiana:

- Ouachita Parish: 17.4%

- Calcasieu Parish: 17.1%

- Tangipahoa Parish: 15%

- Ascension Parish: 14.5%

- Rapides Parish: 13.2%

Negative equity concentrations increase default risks for servicers and can slow resale activity, especially if prices soften or severe weather events affect local housing stock.

Foreclosure and unemployment hotspots

ATTOM reported that one in every 1,211 homes nationwide were in the foreclosure process in the first quarter of 2026.

The highest foreclosure rates among the 580 counties analyzed were:

- Liberty County, Texas: one in every 55 homes in foreclosure

- Baltimore City, Maryland: one in every 294 homes

- Dorchester County, South Carolina: one in every 352 homes

- Kaufman County, Texas: one in every 361 homes

- Pueblo County, Colorado: one in every 368 homes

The national unemployment rate stood at 4.4% in February, according to the U.S. Bureau of Labor Statistics. Several agricultural and tourism-heavy counties posted notably higher jobless rates:

- Imperial County, California: 17.6%

- Yuma County, Arizona: 11.7%

- Tulare County, California: 11.5%

- Merced County, California: 10.9%

- Monterey County, California: 10.8%

For servicers and warehouse lenders, the overlap between high unemployment and elevated foreclosure rates represents the key stress zone to watch as forbearance and loss-mitigation pipelines evolve.