Recently, an activist organization called the Center for Investigative Reporting, under the banner of Reveal News, wrote a story lobbing accusations at some banks and mortgage firms of engaging in discriminatory lending practices. Addressing concerns around discrimination is important and this discussion around the issue is long-standing as the nation works to meet the housing needs of American families. Therefore, publishing factual, complete data is critical so the topic can be discussed based on the merit of the facts and without bias.

The story that Reveal produced left out critical information in what seemed to be a blatant attempt at sensationalism and clickbait. Stunned by the audacity of the authors to cherry pick data and facts in an effort to substantiate their pre-determined conclusions, the Mortgage Bankers Association responded to their story with this blog post.

Rather than simply declare this “fake news”, as that term is so misused today, it’s important to lay out some of the data that this organization ignored in their prejudicial effort to smear mortgage lenders who actually are abiding by underwriting standards created by the federally-related mortgage entities that insure the loans or buy them. This will require an understanding of the Home Mortgage Disclosure Act, the roles of Freddie Mac and Fannie Mae, as well as the roles of Federal Housing Administration, Department of Veterans Affairs and Department of Agriculture, as well as the Consumer Financial Protection Bureau.

The Home Mortgage Disclosure Act requires almost all lenders to report a variety of data to both the federal banking agencies and the CFPB each year that shows detailed loan-level information about mortgage applicants, including information about ethnicity and action taken – whether the application was approved, denied, or withdrawn. Lenders also report information about loan characteristics, including loan amounts and whether the loan is insured or guaranteed by the FHA, the VA, or the Rural Housing Service (a division of the Department of Agriculture). These programs are specifically designed to provide federal guarantees on loans to low- and moderate-income families and first-time homebuyers who have difficulty saving for larger down payments and may have less than perfect credit.

At the outset, Reveal News failed to include any of these federally-backed loans in their analysis. By doing so they simply removed and ignored one the primary sources of mortgage financing for minority homebuyers, skewing the data and giving the wrong impression to the reader.

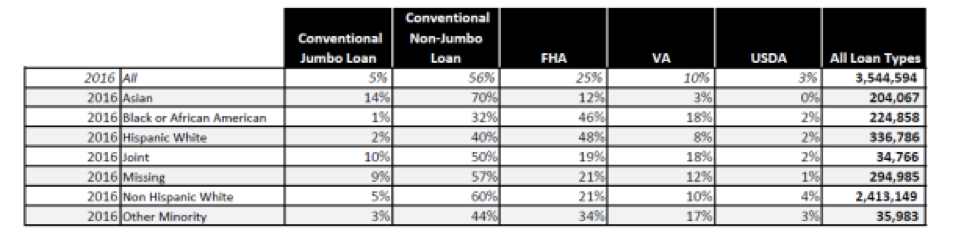

Just look at the table below.

(Click to enlarge)

According to the 2016 HMDA data, conventional loans accounted for just 33% of all loans made to African-American borrowers and 42% of loans to Hispanics. FHA, VA, and USDA loans accounted for two-thirds of all loans to African-American borrowers and more than half of loans to Hispanics, yet Although MBA made this point to the reporter prior to publication, Reveal purposefully excluded all these loans from their analysis in order to construct an argument that lenders don’t serve minority borrowers. Reveal has suggested that FHA, VA and RHS loans are somehow less advantageous to borrowers, but let’s look at the facts.

One might ask, why do minority borrowers rely so heavily on the FHA/VA/USDA programs to buy or refinance their homes? There are several reasons, but here are a few.

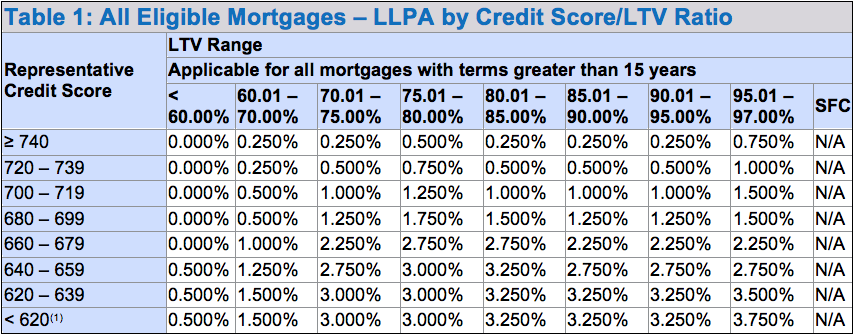

FHA allows smaller down payments at interest rates generally lower than conventional loans, while VA and RHS guarantee loans with no down payment required. On the other hand, Fannie Mae and Freddie Mac, the primary provider of conventional non-jumbo mortgages, use risk-based pricing that charges significantly higher fees to borrowers with lower down payments and lower credit scores (see Fannie’s loan level price adjustment grid). These fees are typically factored into the borrowers’ interest rate, resulting in higher interest rates for conventional loans for those borrowers that lower savings for down payments, or have less than pristine credit, or a combination of these issues.

(Click to enlarge)

So, while FHA charges no additional fees for a 3% down loan (regardless of credit score), the GSEs charge more. Fannie Mae, for example, charges an additional upfront fee of 3.5% of the loan amount (350 bps) for loans at 97% loan-to-value with a FICO score between 620-639. On top of that fee, homebuyers must also pay for private mortgage insurance. In comparison, a borrower putting down 20% with a FICO score above 740 pays an additional .25% (25 bps) and has no additional mortgage insurance fee. So, for many borrowers, especially with lower levels of savings or lower FICO scores, FHA is simply less expensive. Similarly, neither the VA nor the RHS programs utilize risk-based pricing, making their loans particularly attractive compared to conventional loans.

These programs also have more generous qualifying standards for borrowers than conventional loans, including higher debt-to-income ratios (or in the case of VA, a residual income standard). Taken together, these traits make government loans particularly attractive for minority borrowers that do not have accumulated wealth from prior homeownership to help them close the affordability gap. Consequently, any analysis of the industry’s efforts to serve minority homebuyers must include government-backed loans.

However, the post-crisis Qualified Mortgage rule from the CFPB adds additional restrictions that can make it harder to get a mortgage for borrowers not at the top to the credit score scales or without large down payments. This too often impacts minorities. Just look at this one set of facts: The median FICO score in 2016 for all Americans, all ethnicities, was approximately 719, the median FICO score in 2016 for African-Americans was 624.

When you look at that one data point, the likelihood for add-on fees or outright denial becomes higher on a conventional loan from either Fannie Mae or Freddie Mac for borrowers with lower FICO scores. While both of the GSEs are working on new ways to reach qualified minority and lower income communities, the HMDA data clearly shows that minority borrowers still more often choose a non-conventional mortgage for their mortgage.

To be clear, there is work to be done to improve sustainable lending options for those who cannot access the dream of homeownership due to underwriting standards of those mortgage investors or for those who are constrained due to the mortgage rules established by the CFPB. Here are just a few areas where the industry is urging policy makers to focus:

- Revise the QM rule to allow lenders to responsibly extend credit to prospective homebuyers not currently given access to mortgages. The current rule imposes too much legal risk on any lender who makes a loan outside the safe harbor. That needs to change. The rule itself is very narrowly written and will restrict home purchase opportunities to minorities simply due to the debt-to-income requirements, leaving lenders little option unless they want to take on huge legal risk. Until all stakeholders recognize the restrictions in a rule written for consumer protection as one that actually restricts lending to these communities, we may never resolve this issue.

- A significant percentage of African-American borrowers with FICO scores below 620, possess “thin file” credit histories, meaning two or fewer reported entries to a credit bureau. Many are otherwise well qualified, they simply lack credit histories, which can be bad for their score. This is also an issue in the Hispanic community where many are “un-banked” and do not use credit regularly. Looking at other forms of credit such as utility bills and cell phone payments, as well as non-traditional auto loans and more as acceptable credit could help. Exploring other credit scoring methodologies that can score millions of Americans not covered by today’s methods, should be explored.

- Opening up documentation standards to a new style of household that may consist of multiple family members contributing to the mortgage payment, cash incomes from multiple jobs less easily documented, and income from roommates are examples here. There has been progress made on these fronts in the conventional market, but more needs to be done.

- Scale and standardize financial literacy education to better prepare future homebuyers to be more credit worthy. Let’s face it, most kids graduate high school with no means of knowing how to manage their personal finances. This is where it needs to start, reaching into communities with financial literacy education and testing, and valuing that in the mortgage approval process is an opportunity for the future – but we will need partnerships from both the private sector and public sector to achieve real results here.

These are just a few ideas to address a complex problem that Reveal failed to take the time to analyze or present in what appears to be just an effort to smear lenders and the industry as a whole.

The real disgrace of irresponsible journalism like this is that it distracts from and undermines the serious efforts of consumer advocates, policymakers, and business stakeholders to address the serious issues surrounding the housing issues faced by minority communities in this country. These writers simply created a story with partial data that fails to recognize the facts. By selectively choosing “conventional loans” only, they purposely hid the full spectrum of lending, especially FHA, VA, and USDA loans which serve the majority of first time homebuyers, including the majority of African-American and Hispanic homebuyers in their home purchases. These writers failed to do the real work in both understanding the types of mortgages made, which are reported to HMDA, as well as the data that is used to make loans to home purchasers in this country. In the process, by conveying this false message, the Reveal story actually discourages more minority families from considering homeownership as a viable option.

Clearly, this was simply a case of an organization identifying the desired headline, creating the desired narrative, and cherry picking the facts to support it. That is why it is offensive to so many who have spent years working to ensure that personal bias is removed from lending rules. The authors and activists behind this effort should be ashamed of such shoddy work. It is unfortunate that they chose the easy, inflammatory path here, as opposed to truly studying the facts and looking to find real solutions.