The serious mortgage delinquency rate decreased in the final quarter of 2017 to the lowest point since the great recession, according to TransUnion’s Q4 2017 Industry Insights Report.

The serious mortgage delinquency rate, or those that are 60 days or more past due, decreased to 1.86% in the fourth quarter of 2017, according to the report.

“Mortgage delinquency rates for Q4 2017 continued to decline, reaching their lowest levels since the recession,” said Joe Mellman, TransUnion senior vice president and mortgage business leader. “This largely reflects recession era defaults having worked their way out of the system and recent originations being underwritten to a very high standard.”

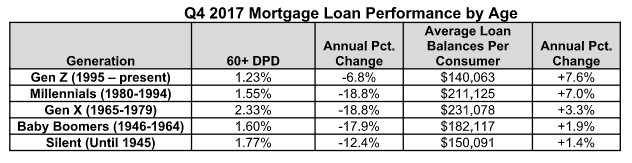

The chart below shows the mortgage delinquency rate decreased across every generation. Millennials and Gen Xers saw the greatest drop in delinquency rates, with Baby Boomers not far behind.

Click to Enlarge

(Source: TransUnion)

The average mortgage debt for all borrowers increased to $201,736 at the end of 2017. This is up more than $7,000 from the previous year.

However, for that same time period, TransUnion found average new mortgage account balances decreased. New mortgage account balances decreased to $228,563 in the third quarter of 2017 from $235,820 in the third quarter of 2016.

This is a reversal from the previous trend where new account balances increased on an annual basis each quarter from the third quarter of 2014 up until the fourth quarter of 2016. TransUnion explained the reason for the increasing mortgage debt even as new account balances decrease.

“This quarter we see an interesting dynamic with seemingly contradictory data points: average mortgage debt per borrower increasing while average new account balances declined,” Mellman said. “There could be multiple factors contributing to this, including cash-out refinancing increasing the average mortgage debt; the drop in refinancing share lowering average new account balances, since average refi size can be larger than average purchase size; and a change in the mix of purchase origination amounts toward lower balances.”