For the better part of a decade, the Texas growth playbook was remarkably simple.

If you wanted scale, liquidity and appreciation, you went to the Texas Triangle: Austin, Dallas–Fort Worth, Houston, and San Antonio and tried to be early to the next ring of rooftops.

Those four metros captured the lion’s share of population and job growth, with national capital following.

That script is changing.

Texas is still outgrowing most of the country, though the pace has cooled. The Dallas Fed notes that the state’s economy is “moderating toward a more historically normal pace” after the extraordinary post-pandemic run-up, with job growth easing even as conditions remain broadly expansionary. Private forecasts expect Texas to remain among the best-performing state economies in 2024 and 2025, but no longer in “everything works” mode.

For builders and investors, that slowdown is less a warning sign than a filter. As capital becomes more selective, markets that can still deliver absorption, pricing power, and entitlement velocity rise to the top of the list. Increasingly, those markets are not the usual suspects inside Loop 1604 or along the Dallas North Tollway. They are places like Weatherford and College Station, secondary markets with real economic anchors and enough pricing headroom to make deals pencil.

Growth normalizes, but demand doesn’t disappear

Step back, and the macro picture still looks attractive. Texas continues to add jobs faster than the U.S. as a whole, though the gap has narrowed as the post-COVID hiring surge fades. Consumer spending and business investment remain solid, even as higher interest rates cool the most rate-sensitive sectors.

In housing, statewide single-family permits are projected to grow modestly in 2025, about 2.5% above 2024 levels, following a period of adjustment to higher financing costs. The Texas Real Estate Research Center expects this to be the second consecutive year of rising starts, signaling that demographic demand and in-migration remain strong enough to support new construction despite tighter affordability.

The nuance is where that demand wants to live. After years of double-digit price growth in premium submarkets, many buyers are no longer willing—or able—to stretch for the same house in the same ZIP code. They are open to trading an extra fifteen minutes in the car for meaningful monthly savings and a different lifestyle. That buyer psychology is the wind at the back of Texas’ secondary markets.

Weatherford: the attainable edge of DFW

Nowhere is this shift more evident than in Weatherford, a city of roughly 30,000 on the western edge of the DFW metroplex. Long known for its courthouse square and cutting horse culture, Weatherford has quietly become one of the country’s fastest-growing affordable suburbs.

In 2025, a national analysis of the fastest-growing affordable suburbs ranked Weatherford 14th in the U.S., one of only four DFW suburbs with fewer than 50,000 people to make the list. The ranking highlighted the city’s ability to combine genuine population growth with home values that remain within striking distance of median incomes.

Current housing data paints a picture of a market transitioning from overlooked to in-demand:

- The average home price in Weatherford is about $350,000, up modestly year over year but still well below many inner-ring DFW suburbs.

- The market is moderately competitive, with homes receiving multiple offers and selling in about two to three months.

- Local analyses show that active new development reshaping the housing stock, with builders responding to population growth by delivering planned communities and modern product.

Buyer behavior is highly instructive for underwriters of new lots. A recent industry piece on Weatherford described the local demand band as concentrated between roughly $350,000 and $850,000, with a strong emphasis on attainable family housing. That range captures move-up households leaving older stock in Fort Worth, as well as first-time buyers priced out of more central submarkets.

On the supply side, Weatherford still offers what core DFW has largely lost.

- Scalable land positions near major infrastructure but outside the most constrained entitlement environments.

- A municipal mindset receptive to growth, particularly in master-planned communities that help the city manage infrastructure and school needs.

- Room for a mix of national, regional, and local builders, rather than a handful of publics dominating the landscape.

For national builders, Weatherford checks several critical boxes: proximity to a major employment engine, visible in-migration, and a buyer profile that supports production-scale communities at price points with meaningful depth. For investors, it offers an opportunity to buy income and appreciation at a discount relative to neighboring submarkets, while benefiting from the halo of DFW’s long-term growth.

College Station: A university market that behaves like a stable metro

If Weatherford is the edge-of-metro story, College Station is the university-anchored growth story. Together with Bryan, it forms a mid-sized metro that has outgrown its college-town label, largely thanks to Texas A&M University’s expansion and a growing ecosystem of research, healthcare, and professional services.

Demand for housing in College Station has been rising steadily. A 2025 market analysis reports that the city has seen a significant increase in demand over the past year, driven by population growth, economic stability, and the continued expansion of Texas A&M. The data support that:

- The average single-family home price is approximately $400,000, reflecting about an 8% increase over the prior year.

- Entry-level homes cluster around $275,000, while luxury properties routinely exceed $750,000, giving builders ample room to segment their product line from student rentals to executive housing.

- Inventory remains tight. Average days on market are near 32, down from 45 a year earlier, and well-priced homes often draw multiple offers.

- Even as some local brokers note a recent tilt toward buyers, with a modest increase in months of inventory, values have largely leveled rather than rolled over.

Compared with Austin or parts of suburban Houston, College Station remains relatively affordable, yet it offers many of the same amenities that attract higher-income residents: strong schools, modern master-planned communities, and access to major metro areas via highway.

For investors, the market offers two distinct yet complementary theses:

- For-sale housing is attracting faculty, professionals, and immigrants seeking a permanent foothold in a stable, growing community.

- Rental product, both traditional and student-adjacent, serving the constant churn of students, staff, and visitors at a major university.

The result is a market in which builders can underwrite both end-user and investor demand, and in which developers can justify amenity-rich projects that serve a broad, resilient tenant base.

Underwriting secondary Texas markets in a slower cycle

For builders and investors trained to chase cranes in Austin or Dallas, reallocating capital to places like Weatherford and College Station requires a shift in mindset. The metrics that matter in a normalized growth environment are slightly different from those that dominate during a boom.

Several principles stand out:

- Follow employers, not just rooftops. In secondary markets, a handful of major employers or institutions can drive a disproportionate share of demand. In Weatherford, that might be regional healthcare and logistics; in College Station, it is Texas A&M and its orbit of vendors and research partners. Underwriting these anchors is as important as underwriting the dirt.

- Prioritize attainable price bands with real depth. The sweet spot in both markets lies where local incomes and out-of-metro buyers overlap: roughly the mid-300s to the high-400s for primary residences, with optionality to go higher for move-up and luxury. That is where absorption is strongest and where builders can still manage incentives and buydowns without destroying margins.

- Lean into entitlement and velocity advantages. Secondary markets often allow developers to assemble larger, more contiguous tracts with less friction and move through approvals faster than in core metros. That time-to-market advantage matters in an environment where interest carry is expensive and exit timing is less forgiving.

- Design for permanent demand, not just the next trade. In a slower macro environment, products tied to deep structural demand—education, healthcare, logistics, and energy—will outperform purely speculative plays. The more a community aligns with those drivers, the more durable its takedown schedule becomes.

The opportunity set: from nice-to-have to core strategy

For years, secondary markets in Texas were treated as optional add-ons – a nice seasoning in a portfolio dominated by the big four metros. In a normalized growth environment with higher financing costs, that hierarchy is being rewritten.

Weatherford, College Station, and similar markets offer something that is increasingly hard to find near the urban core:

- Buy-in points that benefit both builders and buyers.

- Enough entitlements and land flexibility to design real communities instead of just subdivisions.

- Economic anchors are strong enough to support multi-cycle investment.

- The macro may no longer deliver automatic double-digit appreciation in the state’s marquee ZIP codes, but the micro in the right secondary markets can still generate outsized risk-adjusted returns.

- For capital willing to follow jobs, universities, and infrastructure rather than just headlines, Texas’ next yield curve is taking shape west of Fort Worth and along Highway 6. This time, the smart money is getting there on purpose.

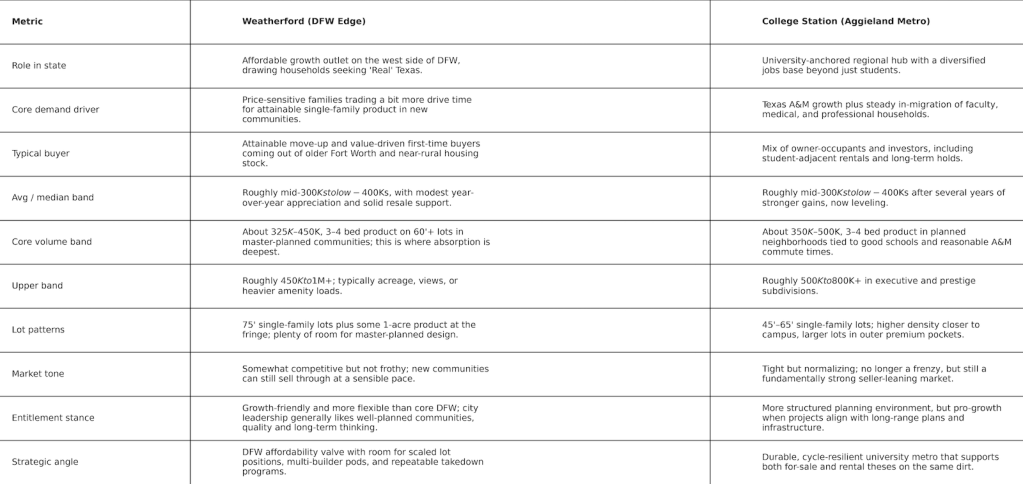

P.S. – A quick homebuilder cheat sheet: Weatherford vs. College Station