The “emerging trends” in housing story over the past decade or more has been a tale of magnitude variations on a theme: constrained supply eclipsed by growing demand.

If there is one conclusion that rises above all others in this year’s “The State of the Nation’s Housing 2026” report, it is that the industry’s challenge has shifted to a new, different, unsettling theme.

Supply is still constrained. But demand, and the demographic bedrocks beneath it, now point to – and beyond – an apogee.

Demand deterioration.

Demand destruction.

Demand deceleration.

You name it.

Demand decline now figures into long-term strategic and business plans that take stock of where we are.

Until now, housing leaders could reasonably assume that demographic demand would eventually absorb whatever product they could bring to market.

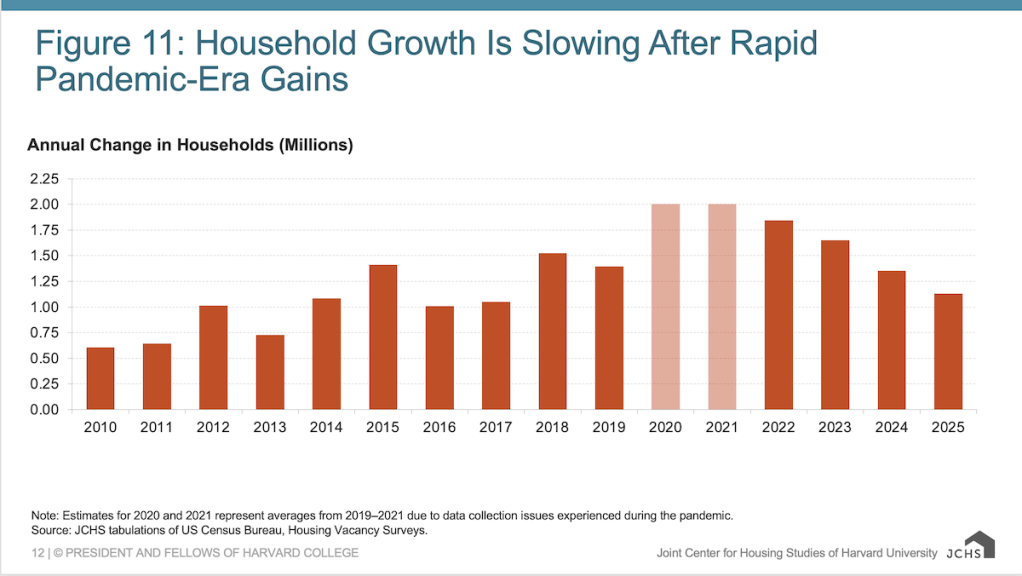

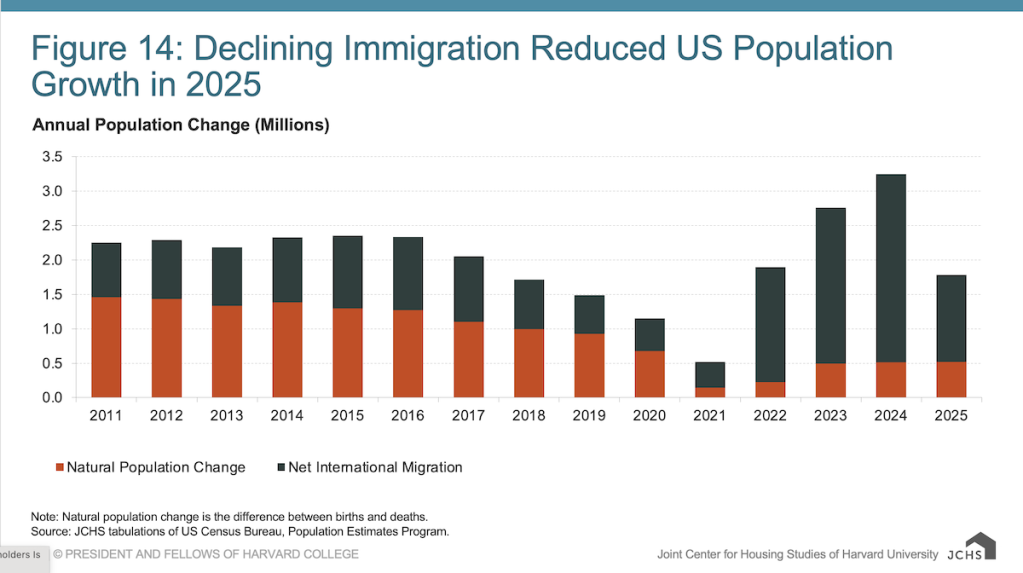

Harvard’s latest analysis suggests that this assumption warrants re-examination. Household growth slowed for a third consecutive year, falling to 1.1 million in 2025 after averaging 2 million annually during the pandemic-era surge. At the same time, job growth weakened dramatically, consumer confidence remained near historic lows, mobility fell to record lows, and immigration slowed sharply.

For builders and developers, the blend of those forces and factors is meaningful. Why? It weighs directly on the industry’s fundamental growth engine: newly-formed households.

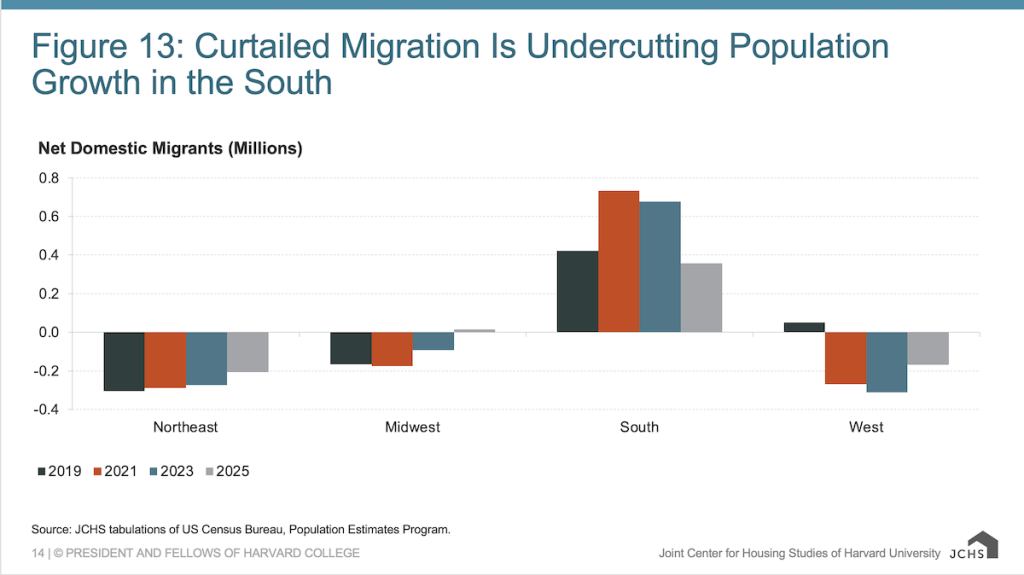

The report documents a market in which fewer young adults are forming households, fewer people are relocating, and fewer international migrants are arriving to fuel household growth. Those trends are not cyclical noise. They represent meaningful pressure on housing demand growth over the next several years.

That reality helps explain many of the operating conditions builders experienced during the disappointing spring selling season of 2026.

10 insights homebuilding leaders need to reckon with

1. Household formation is slowing materially.

The housing industry’s largest long-term demand driver weakened for a third consecutive year. Household growth has effectively returned to pre-pandemic levels after the extraordinary surge of 2020 and 2021.

2. Immigration is becoming a major housing demand variable.

Harvard projects net international migration could fall to roughly 321,000 people in 2026, dramatically below historical norms. That shift has implications not only for household growth but also for labor availability across construction and building products sectors.

3. Mobility has effectively frozen.

Only 11.2% of households relocated in 2024, a record low. Existing homeowners remain locked into low mortgage rates, reducing both resale inventory and move-up demand.

4. Builders are already adapting their product.

The industry’s response to affordability pressures is clearly visible. Builders are delivering smaller homes, smaller lots, more townhomes, and more incentive-driven financing packages. Homes under 1,800 square feet increased their share of completions significantly, while townhomes reached 18% of single-family completions.

5. Unsold inventory is becoming a constraint.

Unsold completed new-home inventory rose 54% over two years and reached its highest level since 2009. That inventory overhang is helping suppress additional starts.

6. Build-to-rent has moved from niche to meaningful demand channel.

Single-family homes built specifically for rental represented 11% of completions in 2025, nearly three times historic norms. Builders increasingly relied on institutional rental demand as owner-occupant demand softened.

7. Multifamily is entering a different phase of the cycle.

The industry is still absorbing the largest apartment delivery wave in decades. New supply helped moderate rents in many Sunbelt markets, but the development pipeline is shrinking as units under construction decline.

8. Affordability remains historically broken.

Even with slowing home-price appreciation, the median existing-home price remains nearly five times median household income. Mortgage payments on a median-priced home remain roughly double where they stood in late 2020.

9. Housing costs now extend far beyond mortgage payments.

Insurance premiums increased 72% between 2019 and 2025, while property taxes rose 31%. Those cost increases are becoming increasingly important purchase-decision variables.

10. The housing shortage increasingly centers on affordability, not simply volume.

The report’s most sobering statistic may be that 11 million extremely low-income households compete for only 3.8 million affordable and available rental units. The nation’s biggest housing shortfall is no longer a generic unit shortage; it is a shortage of attainable housing.

Three opportunity areas emerging for builders

The report also highlights several strategic opportunities for builders, developers, capital partners, and suppliers willing to adapt.

1. The attainability innovation race

The companies that figure out how to deliver attainable housing at scale stand to capture disproportionate market share.

The report repeatedly points to the widening gap between what households can afford and what the industry can economically produce. That gap creates opportunity for innovation in lot design, floor plans, off-site construction, automation, value engineering, and entitlement efficiency.

2. Build-to-rent becomes core strategic, not reactive tactical

Institutional rental demand is no longer merely a backstop during slow sales periods.

The growth of build-to-rent suggests a structural evolution in how housing is delivered and consumed. Builders capable of serving both for-sale and for-rent demand channels may enjoy greater resilience during future market cycles.

3. Remodeling and existing-housing preservation

The aging housing stock is quietly becoming one of housing’s largest business opportunities.

Owner improvement spending reached $376 billion in 2025 and now rivals spending on new single-family development. With owner-occupied homes reaching a median age of 42 years, demand for repairs, retrofits, resiliency upgrades, energy improvements, and modernization appears likely to remain durable.

Three risks that could reshape the next 36 months

1. Structural demand deceleration

The combination of slower household growth, weaker immigration, lower mobility and diminished consumer confidence suggests that the industry’s long-assumed demand floor may be lower than many business plans assume.

2. Housing cost escalation beyond purchase price

Insurance, taxes, utilities, resiliency requirements and climate-related expenses increasingly influence buyers’ decisions. Builders who focus solely on purchase-price affordability risk overlooking the growing importance of monthly ownership costs.

3. Climate and disaster exposure

Harvard’s report identifies climate risk as a housing-supply issue as much as an environmental one. Billion-dollar weather disasters continue to rise, while federal disaster-recovery and mitigation frameworks face growing uncertainty. Those pressures could reshape land values, insurance availability, development economics, and geographic growth patterns across many markets.

Make no mistake …

What to learn from The State of the Nation’s Housing 2026 is that housing’s challenge is shifting from whether America needs more housing to whether it can produce housing that aligns with what households can afford.

Builders spent much of the past decade responding to undersupply. The next phase may require something more difficult: aligning product, land strategy, operations, capital structures, entitlement processes, and technology investments around a consumer whose purchasing power has weakened even as housing costs remain historically high.

The industry’s leaders have already begun that transition through smaller homes, smaller lots, incentive-driven financing, build-to-rent partnerships, and operational efficiency initiatives. Harvard’s report suggests these moves are not temporary responses to a soft market. They may instead mark the early contours of housing’s next operating model.