Tuesday’s new home sales report missed expectations and had negative revisions, which isn’t surprising given this sector of our economy simply can’t handle higher mortgage rates. The housing market is in a recession, something that the homebuilders and the National Association of Realtors now agree with me on, as this recent CNBC clip shows.

This means that the builders are done building new single-family homes until they make sure they can get rid of their 10.9 months of supply in an orderly manner. That could happen if lower rates spur more demand, but today the 10-year yield is still at 3%. So for now, the builders will take their time with the homes under construction and make sure they offer enough incentives to unload the new home supply they’re dealing with.

From Census: Sales of new single‐family houses in July 2022 were at a seasonally adjusted annual rate of 511,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 12.6 percent (±16.9 percent)* below the revised June rate of 585,000 and 29.6 percent (±10.9 percent) below the July 2021 estimate of 726,000.

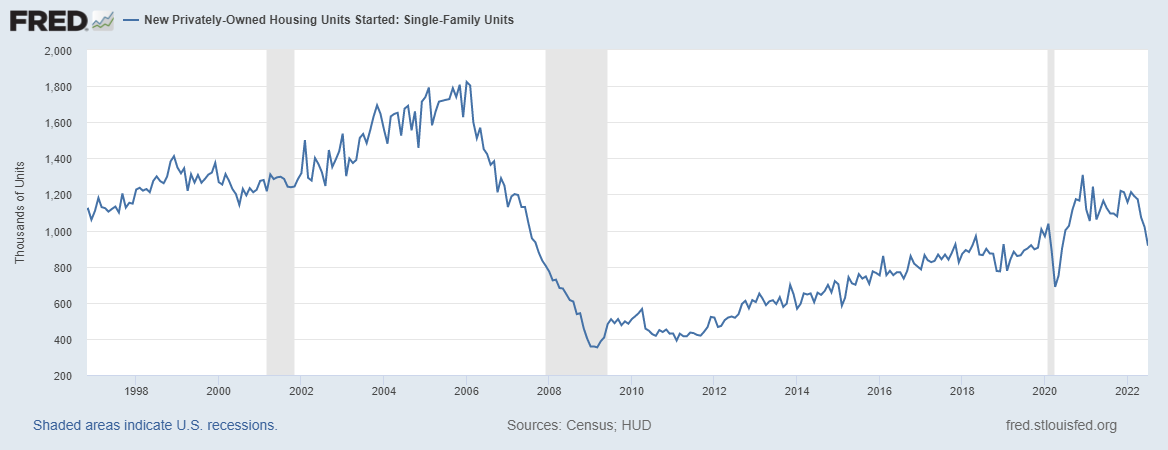

Over the years, I have tried to emphasize that the housing market in the U.S. can’t have a credit sales boom like we saw from 2002-2005. This means we won’t be working from record-breaking demand of high sales like we did at the peak of 2005. After all, sales levels are already low historically for new homes. Tuesday’s new home sales report shows only 511,000 new homes sold. This is below the recession levels of 2000 and back to 1996 levels.

The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4 million, with a significant overproduction of single-family homes in relationship to the natural demand curve of new home sales.

After the peak in 2005, new home sales fell by 82% from peak to bottom and then had the weakest housing recovery in the next expansion. We had missed sales estimates in 2013, 2014 and 2015. Also, we had a supply spike in 2018, which caused builders to pause construction — and that was with rates only getting toward 5%. Today, rates near 6% are simply too high for the product they sell to the public.

From Census: The seasonally‐adjusted estimate of new houses for sale at the end of July was 464,000. This represents a supply of 10.9 months at the current sales rate.

You read that right: 10.9 months! We are almost back to the monthly supply level at the peak of the housing bubble crash! Does this mean massive supply will be coming to the market any second now?

Nope, it’s a different story this time around. First, we haven’t had the same housing supply production as the run-up in the housing bubble years, primarily driven by single-family housing. This time, we have less production of homes and more multifamily construction.

Also, because housing completion data has been so bad in the past few years, it’s taking forever to finish these homes. This means we have a lot of homes under construction or that have not even started. The numbers are historic.

- 1.06 months of supply are finished products

- 7.33 months of supply are under construction

- 2.51 months of supply hasn’t even been started yet

My rule of thumb for anticipating builder behavior is based on the three-month average of supply:

- When supply is 4.3 months and below, this is an excellent market for the builders.

- When supply is 4.4 to 6.4 months, this is just an OK market for the builders. They will build as long as new home sales are growing.

- The builders will pull back on construction when the supply is 6.5 months and above.

The housing construction cycle is over, but the builders will finish their homes under contract and hope rates will fall soon to lock up buyers. Then they will deal with building more single-family homes, and if rates stay high, it will be interesting to see what occurs. If rates fall back toward 4%, the housing landscape will change.

From Census: The median sales price of new houses sold in July 2022 was $439,400. The average sales price was $546,800.

With housing post-2020, home sellers and homebuilders had a lot of pricing power and pushed it on the consumer because they could. This was much different from the previous expansion.

Now the trick for the builders is figuring out how much they need to discount to get buyers to buy the homes under construction. It’s more complicated with mortgage rates near 6% than with mortgage rates near 4%. However, this is on them — they had pricing power, and just like home sellers in America, they pushed it to make a lot of money in the short run.

The aftermath of higher rates is that homebuilder confidence in selling homes to make money has collapsed. When I raised my fifth recession red flag in June tied to housing, it was before the big collapse in the home builder sentiment.

As you can see below, this confidence index took a waterfall dive recently, which shouldn’t be too surprising considering how fast rates rose on the builders.

All in all, not a shocking report. This year, the housing market entered a recession tied to more traditional recessionary realities. Home sales are falling, production is falling and incomes in the sector are falling. We have seen job losses in the mortgage and real estate sector, but not in the construction labor sector yet, as they need to finish up many homes in construction and those they haven’t started.

This is much different than the credit leverage boom and bust of housing in 2005, but it’s still a housing recession.

We’re covering this important topic at our HousingWire Annual event Oct. 3-5 where Logan is a featured speaker. Register here to join us in Scottsdale, Arizona.