Mortgage delinquencies declined by 1 percent in February from December 2008, when in the past during the December to February season, delinquencies have declined an average 6.5 percent, according to a monthly Mortgage Monitor Report released Friday by Lender Processing Services Inc. (LPS). Total February delinquencies are now at 8.37 percent. The data also show a dramatic acceleration in the pace of foreclosure starts for non-agency jumbo prime mortgages, LPS said. February posted the largest single-month percentage increase in foreclosure inventories since December 2007, LPS said. The February foreclosure rate increased 8.2 percent month-over-month and 75 percent year-over-year, to a total rate of 2.23 percent. Non-agency foreclosure sales continued a downward trend in the month, while FHA foreclosure sales followed suit, ticking down toward record lows. “The moratorium on Fannie Mae (FNM) and Freddie Mac (FRE) foreclosure sales expired on January 31 and was reinstated on February 13, to continue through the end of March,” LPS analysts said in a media statement regarding the report. “During the two-week period when the moratorium was lifted, agency foreclosure sales approached all-time highs.” Agency foreclosure starts from December to February surpassed FHA foreclosure starts, although private-party foreclosure starts still hold the highest pace of starts. Subprime is still king of the roost when it comes to foreclosure starts by product, though the category did show a bit of a decrease in the past month. Option ARMs soared past Alt-A in terms of foreclosure starts, although both hold at historic highs. RealtyTrac in mid-March reported surprising data: foreclosure filings, which were driven by new defaults and reported REO inventory, surged for the month, although actual foreclosure sales had fallen. The foreclosure halts in place at the GSEs and some major banks kept many properties from going through the foreclosure sale process for a time, but they did nothing to keep borrowers from entering the process after becoming delinquent. The effect is a backlog of properties somewhere along the way from a notice of default to becoming REO. That backlog, once the stops are removed, leads to an influx of foreclosure sales. LPS’ data show the volume of first payment defaults — when a borrower becomes delinquent defaults without a single payment — on Federal Housing Administration-insured mortgages has reached historic highs recently and spiked up again in December after November’s lull. When taken with historic highs of FHA originations as a percentage of the total volume of originations, this observations loses some of its shock. As LPS noted, “there has been no observed increase in the rate of first-payment defaults for either FHA or non-government loans.” LPS, which also studies the prepayment rate — or the rate of refinance, which treats a mortgage in a loan pool as paid-in-full, although the loan has not disappeared but simply moved to a different pool — found that the rate of prepayment among borrowers current on payments has spiked considerably from December to February and now sits at a high not seen in the reported data from January 2007. The prepayment rates among delinquent borrowers, however, has not changed much in the last few months and are lingering far below the rate for current borrowers. These data suggest delinquent borrowers are not able to refinance as easily as current borrowers. Additionally, LPS found that refinance activity in the last several months has been “concentrated primarily in the highest FICO category” of 720 plus. “Prepayments have continued to increase significantly, but refinance liquidity is concentrated most in borrowers who need help least,” LPS said. Modification, an alternative to refinance in which the borrower can reach some other repayment plan with the lender, did not fare particularly better in recent months, according to the data. The rate of recidivism — or re-default after modification — has improved little. According to LPS, continued recidivism rates exceeding 50 percent six months after modification attest to the “quality” — or lack thereof — inherent in the volume of modifications made during the fourth quarter 2008. A look into roll rates — or the rate at which loans move from one stage of lateness or delinquency to another, ultimately to 90 plus days delinquent or real estate-owned — shows a startling trend that has developed after the burst of the housing bubble. Overall, the volume of loans rolling from better to worse has outpaced those rolling from worse to better for much of 2008. A brief glance at February’s data would almost give the impression that worse-to-better roles are racing to catch up, meaning borrowers are finding some means of payment. While essentially this assumption is true, LPS was quick to point out that the worse-to-better roll rate included a recent surge in refinanced mortgages, which shows up as an influx of prepayment and pulls a mass of borrowers out of the delinquent buckets and into the paid-in-full bucket. “When the prepayment impact on roll rates is removed, the trend toward higher rates of loans improving in status is eliminated and there is no observed increase or decrease in that category over the last several years,” LPS said. The six-month increase in the percentage of loans rolling from 30 days delinquent to 60 days delinquent — or from bad to worse — was highest in the Anchorage, Alaska metropolitan statistical area (MSA), followed by the Seattle-Bellevue-Everett, Wash. MSA and the San Francisco-San Mateo-Redwood City, Calif. MSA. Taking the middle slots of the top 10 MSAs were New York-White Plains-Wayne, N.Y.-N.J.; Santa Rosa-Petaluma, Calif.; Edison, N.J. and Lake County-Kenosha County, Ill.-Wis. The bottom of the top 10 list filled out with an Oregon-Washington MSA and another California and New York MSA. Jumbo Prime took the cake in terms of which product showed the highest deterioration in 30-to-60-day roll rates from February to July 2005, followed by non-agency conforming prime. Read the statement and full report. Write to Diana Golobay at [email protected]. Disclosure: The author held no relevant investment positions when this story was published. Indirect holdings may exist via mutual fund investments. HW reporters and writers follow a strict disclosure policy, the first in the mortgage trade.

Jumbo Prime Foreclosure Starts Spike: Report

Most Popular Articles

Latest Articles

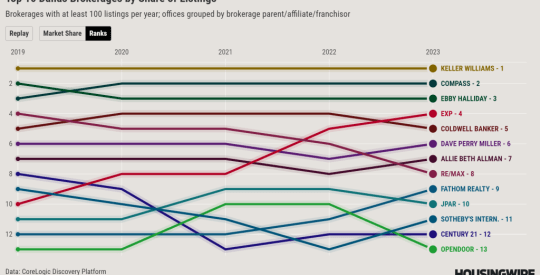

Special report: The brokerages gaining or losing market share in Dallas

Few cities have benefited as much from the trend of Americans moving south as Dallas, which added 170,000 residents in 2021 and 2022.

-

Technology’s role in rental property investment market

-

Best real estate continuing education schools for quick and easy license renewal in 2024

-

CoStar Group finds success through the sale of Homes.com memberships

-

Kevin Sears pulls back the curtain on NAR’s commission lawsuit settlement

-

A look back at HousingWire’s 2023 Marketing Leaders