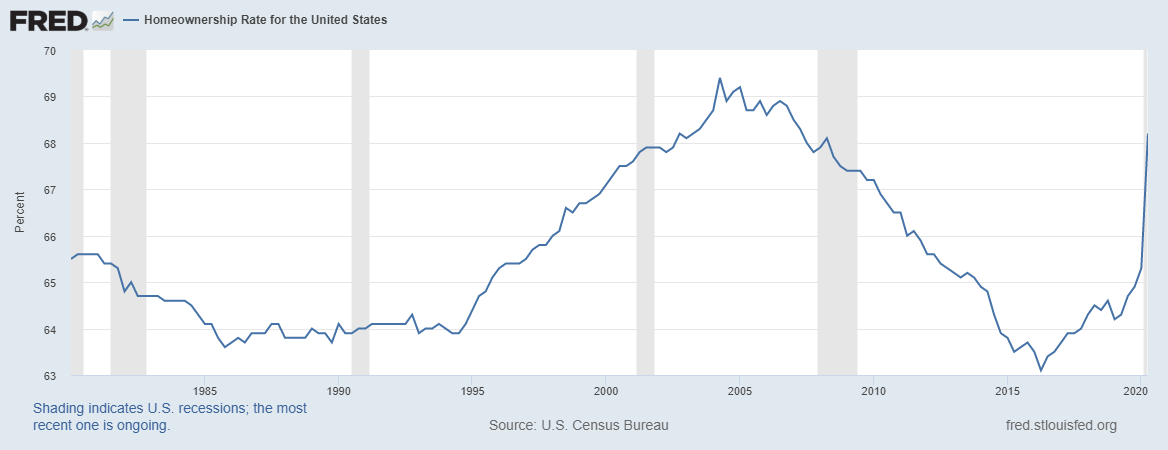

On Wednesday, the Census Bureau reported a surprise increase in the homeownership rate, up from 65.3% to 67.9%.

This increase challenges the long-standing thesis that college-educated Americans are too broke to own homes due to the financial burden of student loan debt.

Lead Analyst

From the Census Bureau: “The homeownership rate of 67.9% was 3.8 percentage points higher than the rate in the second quarter 2019 (64.1%) and 2.6 percentage points higher than the rate in the first quarter 2020 (65.3%).”

I should start by saying I don’t think this number will stick. Any massive deviation from a historical trend needs to be questioned and the question I am asking (tongue in cheek) is: Has COVID-19 somehow impacted the accounting data?

Having said that, even when the data is corrected, in time the report will show that once Millennials get to the proper age to buy a home, a portion of them will do so.

Also, we are officially in the window of 2020-2024!

In the previous expansion, I talked about how homeownership rates should bottom out around 62.2%-62.7%. We got as low as 62.9% before the rate started to move higher. Last year I gave a rationale for homeownership rates to reach 66.21%. Oh, the trolling I got for that forecast!

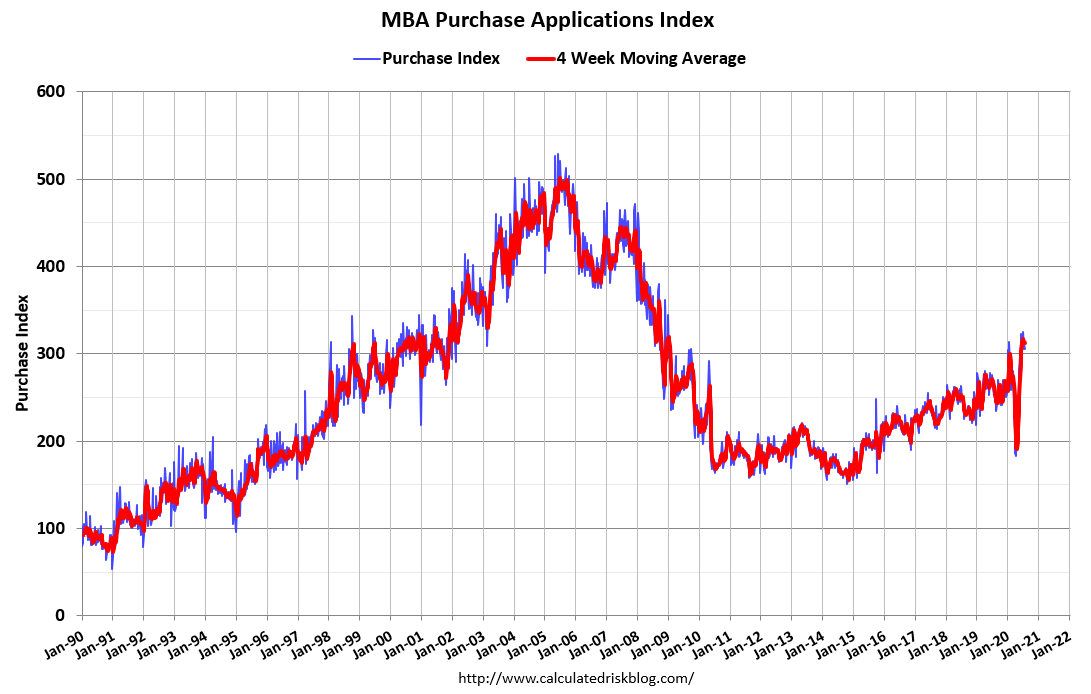

My thesis for 2008-2019 was that we would have the weakest housing recovery ever. My thesis was that we would not have the demand to drive the Purchase Application Index to 300 or over until the years 2020-2024. This year, as if on cue, the purchase application index reached 300.

Speaking of the Mortgage Banking Association’s purchase application data, it is up 21% year over year this week. That is 10 straight weeks of positive year-over-year growth and nine straight weeks of double-digit year-over-year growth. The last four weeks with this data line has shown growth of 21%, 19%, 16% and 33%.

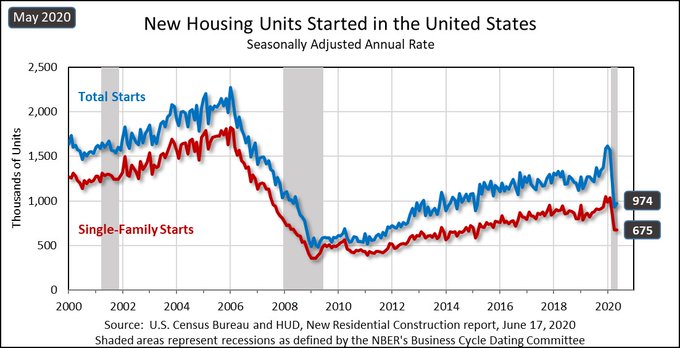

I also predicted that total housing starts would not reach 1,500,000 until the years 2020-2024. We have not had the demand to warrant that amount of building. We have yet to start a year with 1,500,000 units built in the previous year, but we are getting there.

Those who have followed my work know that I have railed against the notion that the student loan debt crisis was holding back housing and that college-educated Americans are now the debilitated class of our society.

Since 2014, we have had steady year-over-year growth in purchase application data. When you look at the actual data on student loan debt, you see that those who matriculate from college have the highest employment rates and the highest incomes. Although they may accumulate student loan debt, they also have the financial capacity to own the debt.

Those who have delinquent student loans owe, on average, $10,000 and did not finish college – and so are not positioned to earn salaries that allow for homeownership. Of course there are many exceptions to this.

Student loan debt is a legitimate financial problem for many — mostly for those who were unable to finish college and reap the career benefits of a degree. But it was never the over-hyped problem for the housing market. I outlined a plan to relieve student loan debt in an article I wrote for Housingwire this year.

I anticipate that the recently published homeownership rate of 67.9% will be revised lower in time. My 66.21% homeownership rate call might not have been bullish enough, and I will gladly accept my error.

However, my main point stands that housing economics are driven by demographics and mortgage rates.

The years 2020-2024 have the largest demographic patch of home-buying aged Americans in history. These demographics will support replacement buyers and any move-up or downsizing buyers just adds more demand into the total numbers.

Since the loan quality from 2010-2020 was better than in the housing bubble years, we will not have any mass scale foreclosures like we saw after the housing bubble burst. For 2021, the forbearance issue will impact housing, but not to the degree some people think. More on this to come.

For now, believe that demographics and low interest rates will be the winning combination for the rest of the year.