#div-oas-ad-article1, #div-oas-ad-article2, #div-oas-ad-article3 {display: none;}

If the first thing you think of when you hear “reverse mortgage” is an Alex Trebek infomercial on late-night TV, you haven’t even scratched the surface of the reverse mortgage market and its potential to bring in booming profits for the lending industry. Older homeowners are sitting on trillions of dollars in home equity that represent a real opportunity in the face of declining purchase mortgages.

Home equity conversion mortgages, more commonly known as reverse mortgages, have been insured by the Federal Housing Authority since February 1988, when President Ronald Reagan signed it into law as part of the Housing and Community Development Act of 1987. The first FHA-backed HECM loan originated in 1989 from James B. Nutter & Company.

Since then, the share of reverse mortgages in the overall industry has seen its ups and downs, but in the current environment the industry is growing, and growing fast.

The National Reverse Mortgage Lenders Association’s Q4 2016 report on senior home equity, published in March 2017, reported a $170.7 billion gain in home equity, bringing the total value to $6.2 trillion.

These gains saw the NRMLA and RiskSpan Reverse Mortgage Market Index (RMMI) reach an all-time high of 221.75, the highest the index has reached in its 17-year history. In a press release, the CEO and president of the NRMLA, Peter Bell, explained that this increase exhibits how equity can be beneficial for retired homeowners and that now is the time to start looking at it as a viable and strategic option for seniors.

“The strong RMMI in the fourth quarter of last year shows that home equity continues to be a valuable asset for homeowners 62 and older,” Bell said. “It’s time for consumers to study what it means to have home equity and to learn about its strategic uses, including how it can be used to support retirement goals.”

Bell further explained that the numbers are also encouraging for future retirees who might be facing a less than pleasant retirement. “The positive trend is also reassuring for homeowners nearing retirement age who are less likely than their predecessors to leave the workplace with a defined benefit plan and also more likely to have long-term debt,” he said.

Additionally, the Department of Housing and Urban Development’s 2015 American Housing Survey reported that 76% of the 11.9 million households led by people age 75 or older own their homes, while the remaining 24% are renters. HUD also reported that for this demographic, the median home purchase price was $53,000, but the median value of this group’s homes was $150,000. This equity position is much higher than for homeowners overall, where the median purchase price was $127,000 and the median home value was $180,000. HUD’s 2015 report also shows that 78% of older homeowners owned their homes outright.

In February, the Urban Institute released a report, Seniors’ Access to Home Equity: Identifying Existing Mechanisms and Impediments to Broader Adoption, which detailed the reasons older homeowners have reservations when considering home equity as a possible source of retirement income.

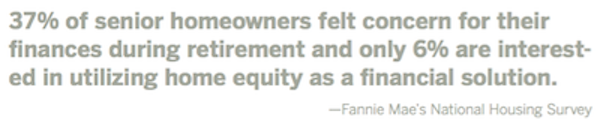

The paper’s data is backed by Fannie Mae’s National Housing Survey, which found that 37% of senior homeowners felt concern for their finances during retirement and only 6% of seniors are interested in utilizing home equity as a financial solution.

With all of this equity available to capitalize on and use to bolster retirement income, why aren’t more senior homeowners taking advantage of products like reverse mortgages?

According to the Urban Institute report, authored by Laurie Goodman, co-director of the Housing Finance Policy Center, and research associate Karan Kaul, these reservations reflect a misunderstanding of how reverse mortgages, home equity lines of credit and other similar financial tools work, and a fear of leaving debt to family members after death. Many people, including seniors, have a preconceived notion about home equity and how it works.

Among many factors outlined, the most important was that there is very limited appetite for tapping into equity, which may be attributed to two things: first, seniors want to avoid going into further debt and risk losing their home; and second, continued advancements in health and medicine allows seniors the ability to work until later in life, deferring the need to tap into home equity.

But some factors for the low participation rate go beyond behavior patterns and medical advancements.

In a blog post featured on Fannie Mae’s website, the authors explained that there are gaps in information and education that contribute to the low rates of equity extraction.

“Beyond these behavioral factors, structural impediments to equity extraction are also at play, including poor financial literacy, the complexity and high costs of some mortgage products, and fear of misinformation and fraud, particularly with respect to reverse mortgages,” the blog post read.

“Post-crisis credit tightening has also affected home equity lending. As varied as these impediments to equity extraction are, they all ultimately lead to one outcome: enormous untapped housing wealth that represents both a potential solution to the financial strains facing some elderly homeowners and a significant untapped market for the housing finance industry.”

#div-oas-ad-article1, #div-oas-ad-article2, #div-oas-ad-article3 {display: none;}

WHAT’S IN THE FINE PRINT?

The decision to tap into home equity requires serious consideration, said Lori Trawinski, a director with the AARP Public Policy Institute. “It means that you’re borrowing money and you really need to think about the implications for that,” she said. “While you’re getting a reverse mortgage, you don’t have to make payments on the loan itself but you’re set to pay all the other fees.”

Many potential borrowers aren’t aware of the additional fees or requirements when signing up for a reverse mortgage. These other fees include the homeowners’ insurance for the property, property taxes, and the cost of any maintenance required on the home during the time of the mortgage.

Potential reverse mortgage borrowers are required to complete a counseling session with a HUD-certified counselor. Trawinski explained that in these sessions the counselor covers other options to consider before completing a reverse mortgage.

“People might want to consider moving,” she explained. “They may find themselves in a home with too many stairs, or need other modifications. Sometimes people consider downsizing or moving to more appropriately sized homes with fewer stairs and better facilities for them and sometimes proximity to relatives is an issue for people and it might be a better option for them to live closer to family members.”

“If it’s a matter of renovating, a reverse mortgage may meet those needs,” she said. “It depends on what the personal financial situation is, and whether they have other resources or not.”

IMPROVING LITERACY

The Urban Institute study also posited that improving reverse mortgage financial literacy by introducing the product to homeowners at a younger age may help increase the likelihood that they will apply for one once they are eligible.

The study’s authors explained that this could be achieved by bringing housing wealth and reverse mortgages into retirement planning.

“Reverse mortgage literacy might also be improved through enhancements to the Federal Housing Administration’s Home Equity Conversion Mortgage (HECM) counseling efforts, via customizing counseling based on the potential borrower’s characteristics and financial needs and by initiating counseling earlier in the borrowing process,” the authors wrote in the blog.

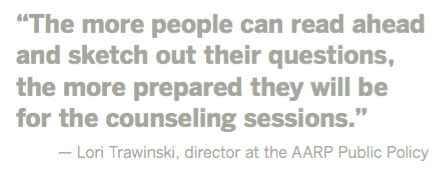

Trawinski said the counseling sessions are only an hour long and that those interested in reverse mortgages should do their research and get familiar with reverse mortgages before the session.

“It’s a lot to take in,” she said. “The more people can read ahead and sketch out their questions, the more prepared they will be for the counseling sessions.” Trawinski said the AARP Public Policy Institute suggests people seek out sources of unbiased information when getting these loans, from someone such as an elder law attorney or a trusted adviser.

“We also encourage including family members to take part,” she added. “It’s a serious decision when you take out a loan and the most important thing is to be fully educated as to what you’re about to do and to what the terms of the loan are.”

Bringing up reverse mortgages earlier in retirement planning may be beneficial, but lenders need to make sure their communications with consumers — including marketing materials — are scrupulously straightforward.

In December 2016, HousingWire’s Brena Swanson reported that the Consumer Financial Protection Bureau handed down civil penalties to three reverse mortgage lenders for deceptive advertising practices. The CFPB said the companies violated both the Mortgage Acts and Practices Advertising Rule, which prohibits misleading claims in mortgage advertising, and the Dodd-Frank Act, which prohibits institutions from engaging in deceptive acts or practices, including in advertising.

The three companies, American Advisors Group, Reverse Mortgage Solutions and Aegean Financial, which also operates as Jubilados Financial and Reverse Mortgage Professionals, signed consent orders acknowledging the actions and penalties and agreed to change loan disclosures, even though none of the companies admitted to committing any wrongdoing.

The bureau ordered the three reverse mortgage lenders to pay a collective civil penalty of $790,000. The bureau’s orders to each business stated that “the company must make clear and prominent disclosures in its reverse mortgage advertisements and implement a system to ensure it is following all laws.”

“These companies tricked consumers into believing they could not lose their homes with a reverse mortgage,” said CFPB Director Richard Cordray in a statement. “All mortgage brokers and lenders need to abide by federal advertising disclosure requirements in promoting their products.”

One of these three companies, American Advisors Group, was hit with the largest penalty – owing $400,000 for its deceptive ads and information kits that assured potential customers that they would have no monthly payments and that with a reverse mortgage they would be able to pay off all debts. In reality, borrowers are still required to comply with all loan terms and could face default and foreclosure if they fail to do so.

One takeaway for lenders is to be especially careful in talking about monthly payments. While it’s true that reverse mortgage borrowers don’t have a monthly mortgage payment, they still have to pay homeowners insurance and property taxes on a regular basis. Any advertising that isn’t clear on this point is likely to land lenders in hot water with regulators.

#div-oas-ad-article1, #div-oas-ad-article2, #div-oas-ad-article3 {display: none;}

LOOKING AHEAD

How does the lending industry capitalize on an untapped multitrillion-dollar market when older homeowners aren’t interested in drawing from equity? Goodman and Kaul’s paper offers several possible solutions, but a recent study by the National Council on Aging, an advocacy organization, suggests that calling it something other than “reverse mortgage” may be the best solution of all.

In the study, which was funded by Reverse Mortgage Funding, the NCOA asked focus groups to compare both home equity conversion mortgages and home equity lines of credit, but did not name either of them. The focus group participants were asked which option best fit their retirement planning needs and 58% of consumers and 43% of financial planners selected a HECM line of credit as the more enticing option.

In the study, which was funded by Reverse Mortgage Funding, the NCOA asked focus groups to compare both home equity conversion mortgages and home equity lines of credit, but did not name either of them. The focus group participants were asked which option best fit their retirement planning needs and 58% of consumers and 43% of financial planners selected a HECM line of credit as the more enticing option.

Once study participants were aware that the unnamed product they liked was a reverse mortgage line of credit, a majority of participants still preferred it over the other and acknowledged a lack of education and understanding about it. To fill this information gap, participants said they were open to advice from a trusted source on using home equity to help fund retirement.

Reverse Mortgage Funding CEO Craig Corn said in a statement that the study shows a demonstrated need for greater education on the topic of home equity solutions. “Continuing to drive education about home equity release products is critical to helping ensure this growing demographic segment is able to retire comfortably and confidently,” he said.

Fortunately, financial advisors are warming up to reverse mortgages as a way to help clients retain and grow investments, a recent CNBC article explained. Financial advisors are recognizing the benefits of taking a HECM line of credit, which is more flexible than a HELOC, and allows seniors to “age in place.”

The CNBC article quoted John Salter, associate professor financial planning at Texas Tech University and a principal of the wealth management firm Evensky & Katz.

“Salter, along with co-authors Shaun Pfeiffer and Harold Evensky, proposed in the Journal of Financial Planning that a line of credit could be used to protect against portfolio declines. If a nest egg suffers deep losses, as many did in 2008 and 2009, retirees can tap their line of credit for living expenses,” the article stated.

For many seniors looking for a comfortable retirement, a reverse mortgage may make the most sense as the best option to boost financial security, especially when the equity pool is so large. Although lenders need to tread lightly when approaching this silver tsunami, the potential upside is huge, paving the way for the next big lending boom.