The rate at which new residential mortgage-backed securities are entering the market is slowing down, with 2016’s rate of RMBS issuance currently tracking well below last year, a new report from Standard & Poor’s Global Ratings shows.

According to S&P’s latest RatingsDirect structured finance report, the overall issuance of structured finance total $27 billion in the month of August, down from $39 billion in July.

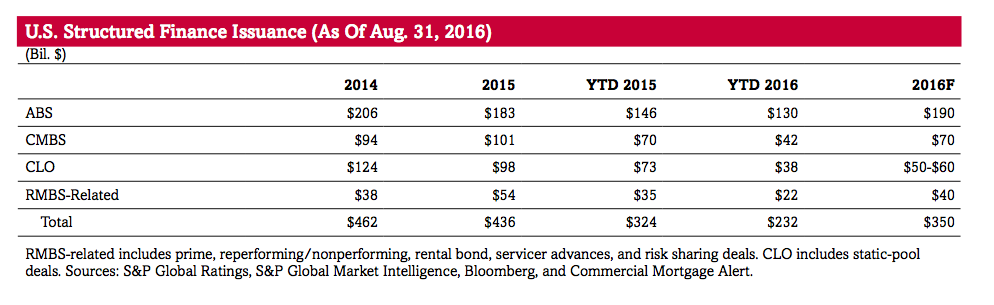

Per S&P’s report, only $3 billion of that $27 billion in new issuance came from RMBS-related bonds, which S&P defines as prime, re-performing/non-performing, rental bonds, servicer advances, and risk-sharing deals.

Further, the agency finds the RMBS issuance in August continued a recent trend as the offerings in August were backed by a “wide variety” of collateral, including prime, non-qualified mortgage, re-performing, non-performing, reverse mortgage, servicer advances, and single-family rentals.

Overall, year-to-date — through August 31 — there has been $22 billion in RMBS-related issuance, compared to $35 billion during the same time period last year.

S&P’s report projects that 2016 will finish with a total of $40 billion in RMBS-related issuance, coming in below 2015’s total of $54 billion and just above 2014’s total of $38 billion.

To be sure, structured finance issuance is expected to pick up as the year comes to a close, but does not expect much of that growth to come from mortgage-related bonds.

In total, S&P’s report shows that year-to-date issuance for all structured finance, which also includes asset-backed securities like auto loans and credit cards, commercial mortgage-backed securities, and collateralized loan obligations, is $232 billion, which is 28% below the 2015 pace.

What's more, overall structured finance issuance is trending higher in the past few months, while RMBS seems to be trending down.

But S&P states that it expects that “recently favorable pricing conditions” should help the market close the gap between last year’s performance and this year during September.

“Overall, we believe the trends of continued low rates and tightening spreads should result in an active September, although recently hawkish comments from the Federal Reserve Bank may contribute some uncertainty,” S&P noted in its report. “Based in part on the expectation of above average CMBS issuance, we think that September 2016 issuance should exceed last September's total of $25 billion and continue to close the issuance gap between this year and last.”

Click the image below to see a chart of the total structured finance issuance for 2014, 2015 and projections for 2016, courtesy of S&P.