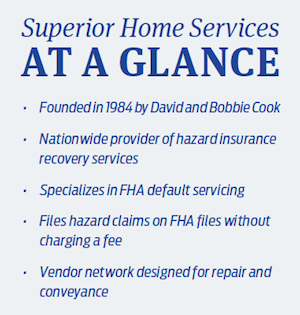

Superior Home Services has specialized in FHA default servicing since the company was founded in 1984. This focus has fueled the company’s drive to innovate in providing hazard insurance recovery services, and has resulted in a unique FHA default solution that remediates properties in light of HUD conveyance standards.

“There is no substitute for experience,” said Patrick Nackley, director of marketing and business development at SHS. “Superior has been focused on the remediation and conveyance of damaged FHA properties in the default cycle for 30 years. We deal with one specific loan type, where many vendors in default servicing will accept any type of loan.”

FHA properties in default operate differently than properties owned by other investors. With Fannie Mae and Freddie Mac, property repair is contingent upon approval. Vendors have to submit a package that gives the GSEs a snapshot of what the property may need, and they may or may not choose to repair. Often they wait to address repairs until the title is in Fannie or Freddie’s name.

HUD operates under a totally different structure. HUD regulations stipulate the use of hazard claims funds when the property must be repaired prior to conveyance. If the use of funds and/or the property is not in a condition pursuant to HUD guidelines, this may result in substantial financial loss to the servicer.

“HUD created a framework where you have the obligation to get a property in conveyance condition before the transfer of title. It is specific to the FHA program,” Nackley said. “Fannie Mae and Freddie Mac require notification of property condition and hazard claim resolution, but do not have as stringent remediation requirements prior to conveyance.”

HUD’s heightened requirements make choosing the right vendor crucial.

“If a mortgagee is going to outsource FHA compliance tasks to vendors, the vendor should manage the process per HUD guidelines,” Nackley said. “Superior only handles FHA files in default. As such, our process and infrastructure are set up specifically to meet HUD guidelines and requirements.”

A SUPERIOR SOLUTION

Superior Home Services has developed a repair contingency program that addresses HUD’s unique requirements while offering the mortgagee a significant benefit. Superior manages the entire process (hazard claim and remediation) on damaged FHA properties and ensures that the bank has a conveyable property, without spending corporate dollars to reach this goal.

“Superior understands the time and expense associated with remediation of these properties,” Nackley said. “Accordingly, no other vendor can better represent the mortgagee’s interests in the hazard claim process and remediation process than Superior.”

“Superior understands the time and expense associated with remediation of these properties,” Nackley said. “Accordingly, no other vendor can better represent the mortgagee’s interests in the hazard claim process and remediation process than Superior.”

Superior’s field services network is designed to be able to identify the difference between insurable damages, and those damages that must be dealt with to satisfy HUD standards for conveyance. Traditional field networks are built to execute high-volume, high-frequency tasks such as mowing grass, securing the property or doing inspections, and are paid according to work orders that specify exactly which tasks need to get done.

In contrast, Superior’s network of vendors is geared to work on bigger jobs where contractors work on draws. Instead of mowing lawns or changing locks, Superior’s vendors may work on one house for a month, performing more significant repairs.

“Many default servicing tasks are high frequency and are triggered and assigned electronically via work orders. Servicers work with vendors to develop processes and operating systems to manage these tasks, maximizing efficiencies to meet demanding timeframes. In contrast, when a servicer needs to address ‘all insurable damage,’ or ‘damage that must be addressed in order to convey a property to HUD,’ a more detailed and programmatic approach is required.

“When you hire Superior to manage insurable repairs, or put a property in conveyance condition, or to do both, we know what needs to be done and how to address those specific, unique issues. Our field network understands the process, understands the expectations of an insurer and those of HUD, can work off a draw system, and has the experience dealing with complex municipal regulatory requirements. Our program is structured to complete substantive repairs,” Nackley said.

“When you hire Superior to manage insurable repairs, or put a property in conveyance condition, or to do both, we know what needs to be done and how to address those specific, unique issues. Our field network understands the process, understands the expectations of an insurer and those of HUD, can work off a draw system, and has the experience dealing with complex municipal regulatory requirements. Our program is structured to complete substantive repairs,” Nackley said.

Many of the people in Superiors’ field network are or have been independent home builders. This kind of knowledge and experience provides Superior field vendors the familiarity to work with municipal regulators as they cure code violations and satisfy code upgrades.

In a recent example of Superior’s work, their office received a call from a client about addressing a re-conveyance in New Jersey. During the process, the property suffered additional damage, and had been cited for code violations by the local township.

Superior’s office was able to file a hazard claim on the new damages and address the code issues with the township enforcement representatives, as well as the building department.

“We were able to, with one estimate, remediate the property to the satisfaction of the local regulatory bodies, offset corporate expense by addressing some of the damage with hazard claim proceeds, and place the property in conveyance condition per HUD standards,” Nackley said.

“As a result, the mortgagee was able to convey the property again within 90 days.”

A CHANGING MARKET

Superior kept its focus on FHA loans even as they became less popular in the run-up to the financial crisis. As subprime loans attracted more and more first-time homebuyers, FHA loans — which had stricter requirements — decreased in popularity.

Now, with tightened underwriting standards and far fewer subprime options, an FHA loan is often the only product that a number of buyers can qualify for. And, because of the higher risk associated with FHA borrowers, the number of defaults on those loans is increasing at a rapid pace.

The National Mortgage Risk Index for Agency purchase loans has soared in the last year, and in April, the market share of high-risk loans outnumbered the share of low-risk loans for the first time ever.

In addition, the cut in FHA’s annual mortgage insurance premium in January has boosted its market share in relation to Freddie and Fannie.

“As the marketplace has changed, what Superior does is now again a very necessary product,” Nackley said. “First-time homebuyers are at a higher risk of default, so inventories of FHA defaults are beginning to rise again. Our company was founded to address this specific issue in the FHA default space.”

Superior’s expertise in the FHA default area ensures that its clients are well prepared to receive the full benefit of the hazard claim in the midst of the current wave of defaults.

“Our clients are ecstatic about our repair contingency program,” Nackley said. “Many default managers in a conveyance department, or sometimes in a REO department, must account for any corporate expenditure in property remediation. Our unique program provides a mitigation and conveyance solution without the need to justify corporate contribution and third-party fees.”