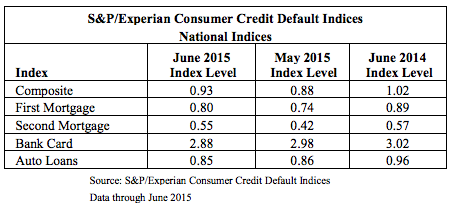

The first-mortgage default rate increased to 0.8%, moving away from last month’s historical low.

The second-mortgage default rate performed similarly and increased 13 basis points to 0.55%, according to the latest S&P/Experian Consumer Credit Default Indices, which gives a comprehensive measure of changes in consumer credit defaults.

Overall, the composite rate posted a 0.93% default rate in June, up five basis points from its historical low in May.

However, David Blitzer, managing director and chairman of the index committee, commented on the report saying, “None of these data are immediate cause for concern. They reflect continued optimism and spending by consumers.”

While the first- and second-mortgage default rate ticked higher, both the bank card default rate and auto loan default rate dipped lower.

Click to enlarge

Source: S&P/Experian Consumer Credit Default Indices

“This report, and the economy’s overall condition, both look a lot like last month,” said Blitzer.

“The economy continues to expand at a modest pace, helped by the 5.3% unemployment rate, a continued low rate of initial unemployment claims, and recent improvements in housing starts. All of these factors should continue to support the current low rate of consumer credit defaults,” he continued.

But Blitzer did note that there are some factors that raise concern for both consumers’ financial conditions and the economy.

“While oil prices are low, they remain volatile as traders and investors weigh the impact of Greece, the agreement with Iran, and the latest bounce and bump in China’s equity market. For consumer spending, oil matters the most of these possible developments. Oil price swings are feeding into consumer prices as seen in the uptick in the June CPI numbers. However, we would need higher inflation for a long time period before it would worry consumers or cause a pause in spending or credit usage,” Blitzer said.

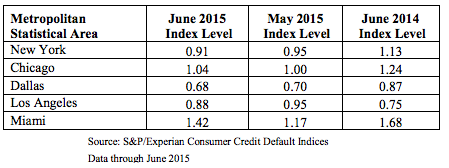

Of five cities reported on each month, both Miami and Chicago increase. The increase in Chicago’s numbers is too small to be a concern. And although Miami’s increase is bigger, the figure does not appear to be an issue, either.

“In the next month or two, data are likely to show Miami in good shape compared with the other cities,” Blitzer said.

Click to enlarge

Source: S&P/Experian Consumer Credit Default Indices