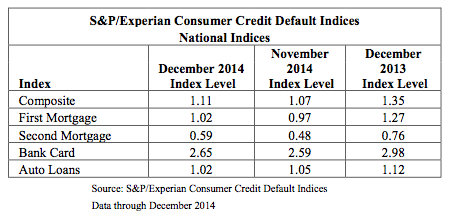

Default rates edged even higher for the month of December 2014, according to the newest S&P/Experian Consumer Credit Default Indices report.

The national composite slightly increased to 1.11%, up from 1.07%, but still down from 1.35% in December 2013.

Meanwhile, the first-mortgage default rate increased for the fifth month straight, rising up from 0.97% in November to 1.02% in December, its largest increase since September 2013. In December 2013, it sat at 1.27%.

The second-mortgage default rate also increased, rising to 0.48% to 0.59% in December. This is still down from 0.76% in December 2013.

Outside of mortgages, the bank card rate increased to 2.65% in December, up from 2.59% in November, while the auto loan rate marginally dropped to 1.02% in December, down from 1.05% in November.

“December was the fifth consecutive month with increasing national consumer credit default rates,” said David Blitzer, managing director and chairman of the Index Committee for S&P Dow Jones Indices.

“Increases also occurred in some recent months in mortgages and auto loans. While the economy is strengthening and consumer spending is gaining, wages have shown little growth. The large drop in oil prices benefits consumers’ disposable income and should limit consumers’ financial stress. Default rates remain very low but could be a cause for concern if the rising trend gains strength,” Blitzer added.

Click to enlarge

Source: S&P/Experian Consumer Credit Default Indices

Click to enlarge

Source: S&P/Experian Consumer Credit Default Indices

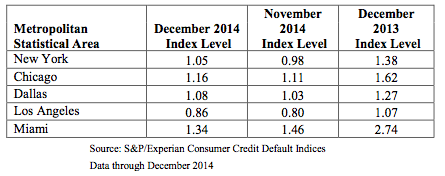

“Chicago, Dallas, New York, and Los Angeles reported default rate increases in December. Across these cities, there is a seasonal pattern with December showing larger than typical increases in default rates, probably associated with holiday shopping and delayed payments,” Blitzer said.

New York witnessed the largest uptick, rising seven basis points from last month’s historic low, to 1.05%. Chicago also increased from its historical low in November, up five basis points to 1.16%.

“Despite the significant increases, all five cities – Chicago, Dallas, Los Angeles, Miami and New York – still remain below rates seen a year ago,” he said.