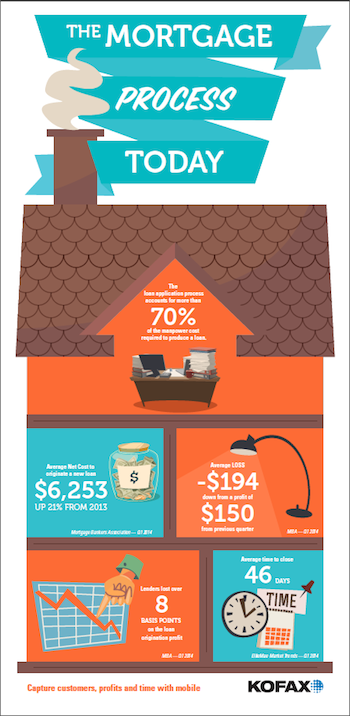

Lenders are under increasing pressure from regulatory burdens and shrinking mortgage volumes. With the cost of origination at an all-time high, finding efficiencies in the process is critical for growth. By utilizing mobile imaging upload, lenders can address one of the most vexing parts of being compliant — getting accurate and timely borrower documentation.

Mobile apps replace the tedious manual process of compiling and entering borrower application information. Borrowers can scan their supporting documents, or take pictures of them with a smartphone or tablet, and the mobile app will extract the data from those sources — which means neither the borrower nor the lender has to manually key in that information.

Automating this step means fewer errors — a critical difference in this era of increased regulatory oversight. A June 2014 article in The Credit Union Times warned lenders that regulators are scrutinizing this part of the process more carefully than ever. “Going forward, focus attention on documentation… Be sure to also document third-party records used to verify debt and income, and document loan file decision-making, which shows the ability to repay or the loan has met QM status.”

Automating this step means fewer errors — a critical difference in this era of increased regulatory oversight. A June 2014 article in The Credit Union Times warned lenders that regulators are scrutinizing this part of the process more carefully than ever. “Going forward, focus attention on documentation… Be sure to also document third-party records used to verify debt and income, and document loan file decision-making, which shows the ability to repay or the loan has met QM status.”

Lenders can see the benefits directly to their bottom line through reduction of errors. One lender, the Bank of Tennessee, saw a 30% improvement in loan processing by using a mobile imaging strategy. A November 2013 article in banktech.com outlined how the bank gained a competitive advantage by using mobile imaging:

“BofT competes with larger regional and national banks that have larger technology resources allowing them to offer superior speed and customer responsiveness as compared to many community banks. Therefore, it was important to enhance our external customer experience by accelerating key internal processes…Better still, our loan officers are now truly mobile, and can offer loan processing and collaboration with our clients from almost anywhere.”

Mobile apps correct and validate borrower data through third-party sources, then deliver it directly into the lender’s system of record. If there are any missing or inaccurate fields, the borrower is notified immediately and prompted to provide other documentation through mobile upload.

The ability to give borrowers a self-service option in providing documentation is a boon to lenders, addressing many of these points:

- No need to chase supporting documents that have been delivered in different formats

- No need to manually type in customer application information

- No need to review the keyed-in data for errors

- No need to hire more staff to ensure accuracy

- No need to spend time contacting the borrower when documentation is missing

- No need to have data directly uploaded into your system of record

Mobile app technology, combined with web portal uploading, eliminates layers of frustration for lenders using a paper-based system, and gives you back precious work time. Plus, it will make borrowers’ experience better as they can engage with you at their convenience and on their preferred device.

Because consumers are looking for immediate, self-service engagement from the companies they do business with, empowering borrowers to upload documents when and how they want becomes a strategic advantage. Among buyers in the 18-to-35 age group, convenience and direct access were the most important factors, after cost, in selecting a mortgage lender.

Mobile imaging upload is a win-win for lenders. It saves you time and money and makes compliance easier, all while increasing borrower satisfaction.

To learn more about how mobile can help your mortgage process, click here: In Pursuit of a Paperless Mortgage.