CFPB RESPA/TILA Rule Reference: 6.1-6.3, page 28-29, CFPB Detailed summary of the rule

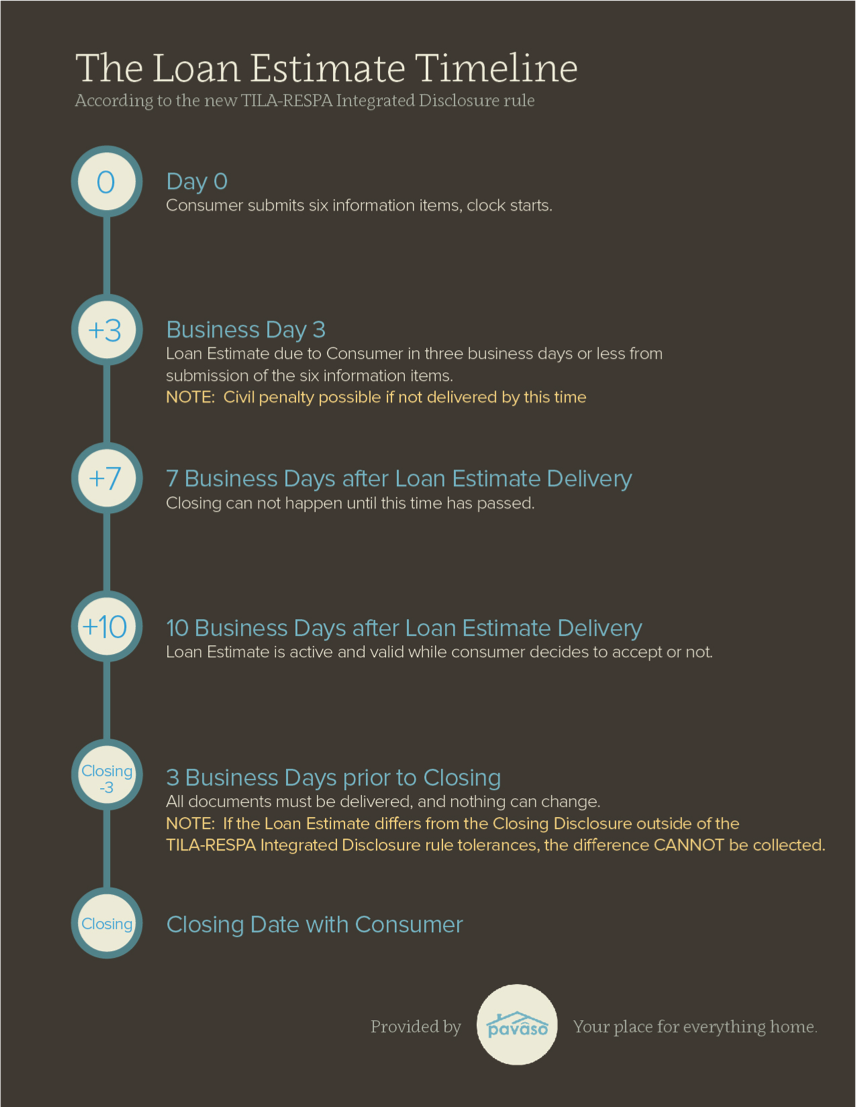

When it comes to the timing around the Loan Estimate form, there are three time windows you need to remember:

3 Days

A common theme with the TILA-RESPA Integrated Disclosure rule is the number three. In the Loan Estimate’s case, the three-day window states that “the creditor is responsible for ensuring that it delivers or places in the mail the Loan Estimate form no later than the third business day after receiving the consumer’s application.”

7 Days

The second magic number is seven. The ruling states that “the creditor is required to deliver or place in the mail the Loan Estimate no later than seven business days before consummation of the transaction.” During this seven-day window, the loan cannot close, so the closing date must be set for after this timeframe.

As with the three-day window, the seven-day countdown begins “when the creditor delivers the Loan Estimate or places it in the mail, not when the consumer receives or is considered to have received the Loan Estimate.”

10 Days

The third time frame to remember is 10 days. After the creditor issues a Loan Estimate to the borrower, they are making an official commitment to the numbers provided for 10 business days. This commitment is meant to give the borrower ample time to analyze their estimate and potentially shop around for a better estimate from another creditor.

The third time frame to remember is 10 days. After the creditor issues a Loan Estimate to the borrower, they are making an official commitment to the numbers provided for 10 business days. This commitment is meant to give the borrower ample time to analyze their estimate and potentially shop around for a better estimate from another creditor.

Take a look at the illustration included here with today’s post, and ask this question — can I meet the potential demands of this timeline with my current process and tools?

These time windows of course have variations and exceptions to the rule, but for most all closings, these will become the standard. As the industry improves its processes to accommodate for these changes, the demand for more efficient ways of communicating between the creditor and borrower will increase. In order to meet these time windows and ensure creditors are not the ones delaying scheduled closing dates, improvements to their daily operations will be essential.

For more information on the impact to the industry and technology solutions that can help your business meet those timeframes, visit the TilaRespa Knowledge Center.

All information and views expressed or implied are provided without warranty and are only the opinion of Pavaso, Inc. Each participant should seek legal representation for legal interpretation of the ruling and the CFPB directly for final instruction and interpretation. The final rule can be found here.